Banking Business and Fund Transfer Transactions: Scope of Bank Regulation (Report of Workshops (2))

Kazutoshi Sugimura *, Masaru Itatani, Masaki Bessho (Bank of Japan)

Research LAB No.17-E-2, March 10, 2017

Keywords: Bank regulation; Fund Transfer Transactions; Collection agency

JEL Classification: G21, G28, G30, K23

Contact: masaru.itatani@boj.or.jp (Masaru Itatani)

- Currently the Ministry of Finance.

Abstract

In Japan, performing fund transfer transactions without a license or registration is subject to criminal sanctions. As the interpretation of the definition of fund transfer transactions has not been clearly established, there may be chilling effects on the development of innovative settlement and payment services. The Report of the Workshops on "Contemporary Financial Transactions and Their Regulatory Treatment" (2016) (the "Report") reviews the intent and purpose of bank regulation, and suggests an approach to determining whether or not a transaction constitutes a fund transfer transaction by properly interpreting its definition, using a collection agency service as a point of reference for legal analysis. The Report also provides a perspective for further discussion on how to implement new legislation with respect to the regulation of fund transfer transactions.Introduction

In Japan, performing fund transfer transactions is considered to fall within the scope of banking business, and is subject to criminal sanctions if carried out without a banking license. However, the Payment Services Act (Act No. 59 of 2009) has partially lifted this ban, and "funds transfer service providers" are now allowed to perform fund transfer transactions as long as the value of such transactions is small. In particular, under the Payment Services Act, those registered as funds transfer service providers may perform fund transfer transactions of up to one million yen notwithstanding Banking Act (Act No. 59 of 1981) provisions concerning the licensing system for banking business (in other words, fund transfer transactions of over one million yen are still handled exclusively by banks).

While the term "fund transfer transactions" is not defined in the Banking Act, the Payment Services Act or other laws, the following definition given in a judicial precedent is usually referred to:

"The phrase 'execution of fund transfer transactions' means accepting orders from clients to transfer funds between remote parties using a system for transferring funds without sending cash directly, or performing such orders upon acceptance of them." (Decision of the Supreme Court delivered on March 12, 2001)

A clear interpretation of the definition given in this judicial precedent may not have been established. For example, jurists have different opinions on whether a service called "collection agency" is within the scope of the relevant Court's definition of fund transfer transactions. If fund transfer transactions are performed without a banking license or registration as a funds transfer service provider, the harshest form of legal remedy, a criminal sanction, may be imposed. This may have chilling effects on the development of innovative settlement and payment services.

History of regulation of fund transfer transactions

Why has the performance of fund transfer transactions been regulated as a banking business in Japan?

In the Bank Ordinance (Act No. 72 of 1890), those who operated a "fund transfer business" were defined as banks. Furthermore, in the Banking Act of 1927 (Act No. 21 of 1927), performing fund transfer transactions was regulated as banking business. This was based on the perception that the essence of banking was a combination of debit business and credit business (i.e. reception and provision of credit). Accordingly, "an operation involving the sale and purchase of out-of-town notes," which in substance equated to fund transfer transactions, was understood as constituting banking business, because drawing notes corresponds to receiving credit and cashing notes corresponds to providing credit.

Under the current Banking Act, "banking business" is defined as business involving either (i) both acceptance of deposits or Installment Savings, and loans of funds or discounting of bills and notes; or (ii) execution of fund transfer transactions. Traditionally, banks have often performed all three operations within the same entity: accepting deposits, lending funds and carrying out fund transfer transactions.

However, these banking operations may be unbundled. They may also be undertaken by entities other than banks if there is a specific statutory basis for doing so. For example, money lenders engage in the business of lending funds, while they borrow funds by accepting loans, not by taking deposits.

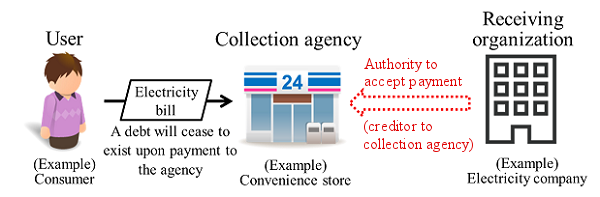

Collection agency

A collection agency service involves transactions whereby a party (the receiving organization) grants authority to receive payments (authority for payment acceptance) to collection agencies such as convenience stores. Collection agency services are in widespread use in Japan, including in the collection of utility payments such as electricity bills. Settlements between receiving organizations and collection agencies are often carried out once or twice a month. Receiving organizations (principals), rather than users, take on the default risk of collection agencies (agents) during the inter-settlement period.

Figure: Collection agency service transaction scheme

As for the relationship between a collection agency service and fund transfer transactions, those who consider that such a service constitutes engaging in fund transfer transactions focus on the fact that the collection agency service is used as a way to "transfer funds between remote parties without sending cash directly." By contrast, those who do not consider that a collection agency service constitutes engaging in fund transfer transactions claim that collection agencies do not receive "orders to transfer funds" from users. Based on the latter interpretation, this service is often provided without a banking license or registration as a funds transfer service provider.

Purpose of bank regulation

Why should banks be regulated? In order to analyze the intent and purpose of bank regulation, this question should first be answered. As shown below, economic discourse provides two explanations as a basis for bank regulation: (1) preventing systemic risk; and (2) intervening in banks' corporate governance.

In the context of the banking system, the concept of "systemic risk" usually refers to "a situation whereby the failure of one bank induces a series of bank failures due to illiquidity." In other words, banks are susceptible to bank runs because they engage in the conversion of maturity through their ownership of illiquid assets while raising funds through demand deposits. If a bank encounters a liquidity crunch or a loss of payment capacity due to a run on that bank or other reasons, this may also affect other banks through a ripple effect. The economics literature illustrates three channels through which systemic risk materializes: (i) a bank run due to psychological associations; (ii) an exposure to non-performance of interbank market obligations; and (iii) a chain reaction through the deferred net settlement system. Bank regulation can be theoretically justified from the viewpoint of preventing systemic risk.

Bank regulation can also be explained in terms of the unique corporate governance structure of banks. In general, creditors are allowed to intervene in the management of corporations in order to mitigate managers' moral hazard problem when corporate performance deteriorates. This intervention functions as a disciplinary constraint on managers. However, the majority of bank creditors are small depositors and do not have the capacity or incentive to collect information on banks' financial conditions. They tend to free ride other creditors' monitoring activities.

If there is an organization which represents the collective interests of small depositors and intervenes in the management of banks when necessary, it will also function as a disciplinary constraint on managers. As large private investors do not always share the same interests as small depositors, a public organization like the government may be a more suitable agency to undertake the monitoring role for small depositors via bank regulation.

Scope of bank regulation

Banking business, which involves both lending and deposit taking, is subject to a set of strict regulations including capital adequacy requirements. The reason for such regulations is to prevent systemic risk from arising in the banking system. In other words, among the three aforementioned systemic risk channels, a bank run on deposits is caused by the acceptance of demand deposits by banks. In addition, exposure to the non-performance of interbank market obligations is due to banks carrying out lending operations. Furthermore, a chain reaction through the deferred net settlement system can be caused by fund transfer transactions.

Keeping fund transfer transactions business exclusive to banks is not the only way to address the third problem. Certainly, small value domestic fund transfer transactions utilize the deferred net settlement system. However, for example, the administrator of the system, the Japanese Banks' Payment Clearing Network, who functions as a central counterparty (CCP), selects member banks and accepts collateral in order to prevent one bank's failure from causing a series of bank failures. If this mechanism functions well enough to reduce systemic risk caused by fund transfer transactions, applying the same set of strict bank regulatory requirements to market entrants who only engage in fund transfer transactions business is not justified.

Further, what if the purpose of banking regulation is to address the monitoring deficiency of small creditors? Banks need to accept funds from clients in advance in order to perform fund transfer transactions. Most clients thus become small creditors to banks, but many of them do not have the capacity or incentive to monitor banks. They may try to free ride other creditors' monitoring activities. They may also face similar bank-related credit risks to the case of small depositors. It may be justifiable that fund transfer transactions as a discrete class have been regulated as banking business, regardless of the bank's involvement in deposit-taking business.

Definition of "fund transfer transactions"

Based on the above discussion, the definition of "fund transfer transactions" established by the aforementioned judicial precedent can be interpreted in a manner compatible with the intent and purpose of bank regulation. In other words, (i) "clients" may be interpreted as "clients who do not have the capacity or incentive to monitor a service provider." Furthermore, (ii) "orders to transfer funds" may be interpreted to mean "requests to transfer funds in a manner whereby the client takes on the credit risk of a service provider which accepts funds through means other than deposits."

Based on this understanding, discussions on the relationship between a collection agency service and fund transfer transactions may be evaluated as follows: first, from the viewpoint of users, who correspond to "clients" above, their payment obligations cease to exist when payments are collected by a collection agency. A receiving organization (principal) which granted the authority to accept payment takes on the credit risk of a collection agency (agent). In other words, users do not take on the credit risk of the collection agency. Therefore, the collection agency service does not constitute engaging in fund transfer transactions when the legal relationship between users and collection agencies is taken into account. Second, as for the relationship between collection agencies (agents) and receiving organizations (principals), receiving organizations may not be deemed "clients who do not have the capacity or incentive to monitor collection agencies" if they are large corporations such as electricity companies. Such clients are expected to have ample resources and incentive to monitor their agents. In such cases, the collection agency service does not constitute engaging in fund transfer transactions.

Perspectives for further discussion

As explained above, the scope of bank regulation may be refined by appropriately interpreting the definition of "fund transfer transactions". If the current state of bank regulation is not compatible with its intent and purpose, however, legislation may be required to address this situation.

In this regard, there is room to reconsider the current framework whereby fund transfer transactions are subject to strict regulation as banking businesses, which is designed to prevent systemic risk. In other words, a coherent approach would be to implement new legislation and exempt from bank regulation those who perform fund transfer transactions without taking deposits, regardless of transaction value. For entities that do not take deposits but perform fund transfer transactions, a different set of regulations focusing on the issue of inadequate monitoring may be established to the extent necessary to protect small creditors.

Reference

- Report of Workshops on "Contemporary Financial Transactions and Their Regulatory Treatment" (2016), to be included in Kin'yu Kenkyu (Monetary and Economic Studies), Institute for Monetary and Economic Studies, Bank of Japan (forthcoming 2017) (in Japanese).

Notice

The views expressed herein are those of the authors and do not necessarily reflect those of the Bank of Japan.