Portfolio Selection by Japanese Households: Investigation Using Japanese and US Households Questionnaire Survey

Yuichiro Ito, Yasutaka Takizuka, Shigeaki Fujiwara (Bank of Japan)

Research LAB No.17-E-5, June 22, 2017

Keywords: Portfolio selection mechanism; relative risk aversion; financial literacy

JEL Classification: C33, D14, D18, G11

Contact: yuuichirou.itou@boj.or.jp (Yuichiro Ito)

Summary

In Japan, cash and deposits continue to be the main financial assets of households. What keeps Japanese households cautious about portfolio allocations? Elucidating the mechanisms behind household behavior is an important issue in discussing the influence of monetary policy. In this study, we outline the analysis by Ito et al. (2017) [PDF 833KB], who examined mechanisms that influence household portfolio selection, using a questionnaire survey for Japanese and US households. The analysis suggests that further improvements in institutional aspects and an increase in financial knowledge, as well as an improvement in market performance and the mitigation of future concerns, are important factors in making the investment environments in Japan more attractive.

Introduction

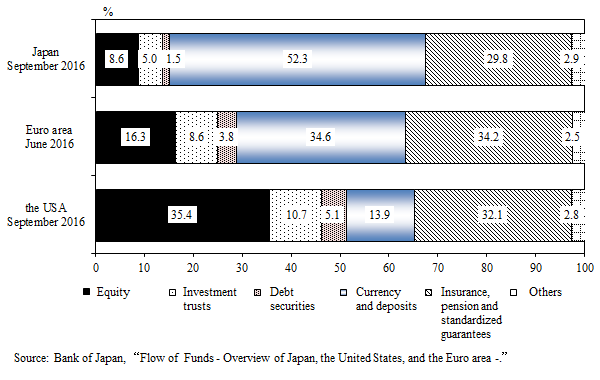

Japanese households hold a low share of risky financial assets such as stocks and investment trusts (approximately 10%), while the share of cash and deposits constitute roughly half of their portfolios (Figure 1). Japanese households are much more cautious about investing in risky assets compared with households in the USA and Europe. Given this, various initiatives in Japan have been undertaken to change households' behavior and promote the formation of households' assets, such as banks' being approved to sell investment trusts. However, cash and deposits continue to be the main financial assets of Japanese households. What keeps Japanese households cautious about portfolio allocations?

Figure 1: Comparison of Household Financial Assets

Since the recent global financial crisis, economic agents, such as firms and households, have become increasingly risk averse, and promoting risk-taking behavior has become a common issue in many countries. Clarifying what keeps Japanese households cautious about portfolio allocations, as well as elucidating the mechanisms behind household behavior, are important issues to consider the influences of monetary policy.

In this study, we outline the analysis by Ito et al. (2017) [PDF 833KB], who examined the mechanisms that influence household portfolio selection, using micro data from a questionnaire regarding financial activities of Japanese and US households. In particular, we reveal what is important for the improvement of Japanese household investment selections, focusing on the differences between Japanese and US households' portfolio selection behavior.

Mechanisms of household portfolio selection

What crucial mechanisms have been considered in households' decisions about portfolio allocations? Merton (1969) and Samuelson (1969), authors of the classical theory of households' portfolio selection, posited that households' optimal proportion of risky assets is determined by the expected value of the excess return on risky assets such as equity (the expected return on risky assets minus the return on safe assets), the standard deviation of return on risky assets (market volatility), and the relative risk aversion (a household's attitude toward risk), with additional assumptions. This theory implies that it is optimal for a household to own some risky assets whenever excess returns are positive, no matter how cautious a household is. However, Mankiw and Zeldes (1991) pointed out that many households own no stock, which implies that other factors may be important in a household's portfolio selection. Other studies have pointed out the importance of saving for income uncertainty (precautionary saving motives), borrowing constraints (liquidity constraints), and the existence of various entry costs for risky assets. They note that regarding the entry costs, structural factors, such as financial literacy and the tax system, have a large effect on a household's portfolio selection.

In Japan, the mechanisms behind this cautious investment stance have been discussed. Based on the classical theory, the cautious attitude of Japanese households toward risk was caused by poor market performance, as well as the fundamental risk-averse nature of Japanese people.1 However, recent research has pointed out that households' cautious attitudes are also caused by various constraints such as liquidity, confidence in financial institutions, entry costs of market participation, financial education, and institutional aspects related to investments (Iwaisako et al. 2015 and Aoki et al. 2016).

Although various reasons have been put forward to explain this cautious attitude toward risk, no consensus has been reached with regard to a decisive factor regarding a household's portfolio selection. Therefore, to explore the background of portfolio selection behavior, an analysis of the aforementioned factors in greater detail is required.

In the following section, we investigate the background of this cautious investment stance, interpreting the results from the Preferences and Life Satisfaction Survey, conducted in Japan and the USA by the Institute of Social and Economic Research at Osaka University. The survey investigated households' market outlook, their characteristics, and the constraints they face. Therefore, it is possible to analyze a household's financial decisions based on portfolio theories.

- Regarding the cautious investment behavior of Japanese households in terms of the behavioral characteristics of households, see Nakajo et al. (2017) [PDF 190KB].

Differences between Japan and the USA

Differences between Japanese and US households regarding asset allocation, as well as factors influencing portfolio selection, utilizing micro data, are discussed below.

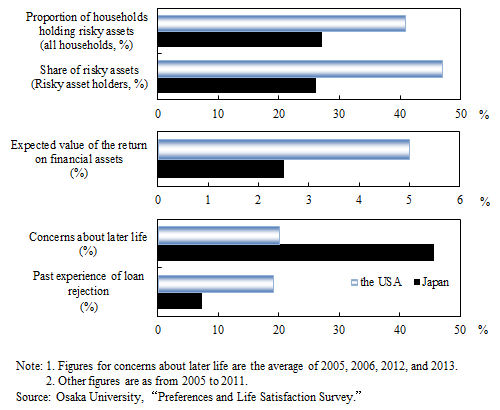

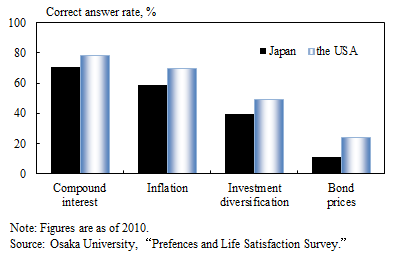

First, statistical analyses confirm that the proportion of households holding risky assets and the ratio of risky assets of risky asset holders are significantly lower in Japan than in the USA. These results testify to the relatively cautious stance of Japanese households vis-a-vis financial investments (Figure 2). Next, as for factors which have a significant effect on portfolio selection, the expected return on financial assets, including risky assets, is relatively low in Japanese households compared to US households. In addition, concerns about later life, which evoke precautionary savings, are clearly higher in Japanese households, while past experience with loan rejections in the USA tends to be relatively high, which probably affect risky asset holding through liquidity constraints. In addition, the proportion of correct answers to financial literacy questions (about compound interest, inflation, investment diversification, and bond prices) tends to be low for every question in Japan (Figure 3)2. It is likely that these differences between Japan and the USA entirely explain the differences in financial risk taking and portfolio selection in Japanese and US households.

- 2Klapper et al. (2015) presented that Japanese households score lower than US households in terms of financial literacy.

Figure 2: Situations surrounding household portfolio selection in Japan and the USA

Figure 3: Correct answer rates vis-a-vis questions about financial literacy

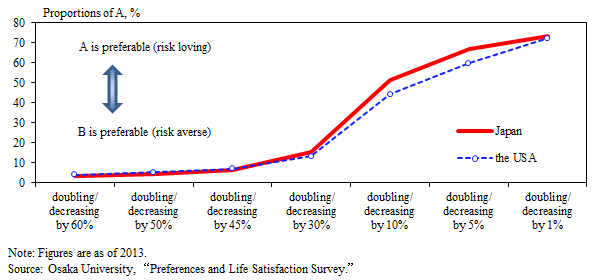

As a consequence, to capture relative risk aversion, which is an important determinant of a household's portfolio selection, we focus on the different attitudes of Japanese and US households regarding monthly salary payments, often used to estimate relative risk aversion.3 Table 1 shows the results of a questionnaire about monthly salary payments. The distribution of responses for both Japanese and US households is similar in shape and does not clearly show that Japanese households are particularly risk averse (Figure 4). Given this result, it is not evident that the "fundamental risk-averse nature of Japanese people influences the difference in household portfolio selection between Japan and the USA" is true.

- 3Barsky et al. (1997) proposed a method that calculates relative risk aversion using a household's attitude toward monthly salary payments.

Table 1: Attitudes toward monthly salary payments

In which of the following two ways would you prefer to receive your monthly saraly?

| Selection 1 | A doubling or decreasing by 60% | B Increasing by 0.5% |

|---|---|---|

| Selection 2 | A doubling or decreasing by 50% | B Increasing by 0.5% |

| Selection 3 | A doubling or decreasing by 45% | B Increasing by 0.5% |

| Selection 4 | A doubling or decreasing by 30% | B Increasing by 0.5% |

| Selection 5 | A doubling or decreasing by 10% | B Increasing by 0.5% |

| Selection 6 | A doubling or decreasing by 5% | B Increasing by 0.5% |

| Selection 7 | A doubling or decreasing by 1% | B Increasing by 0.5% |

Figure 4: Differences in risk attitudes toward monthly salary payments between Japanese and US households

However, the estimated levels of relative risk aversion evidently vary depending on the measurement methods employed and the nature of the risk. In addition, when we discuss differences in the national character of Japan and the USA, how much consideration should be given to demographic differences and the social security systems of the two countries. Considering these points, the result shown in Figure 4 cannot necessarily deny the view that "Japanese households are risk averse."

Background of the differences in asset allocation between Japanese and US households: A quantitative analysis

How can we comprehensively evaluate the background of the difference in asset allocations between Japanese and US households? In this section, we quantitatively analyze households' portfolio selections, considering various factors. In line with the previous literature, we separately analyze (i) how much to invest in risky assets when assuming possession of risky assets (conditional share) and (ii) whether or not to own risky assets (participation rate). We explore the influence of various factors, such as the factors of the classical theory (expected excess return on risky assets, market volatility, and relative risk aversion), liquidity constraints, precautionary saving motives, and entry costs.

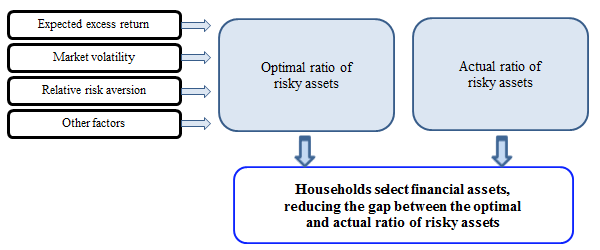

First, we analyze mechanisms that determine conditional share. Specifically, we model households' behavior, assuming that the unobservable, optimal proportion depends on various determinants such as the factor of the classical theory. We focus on Japanese and US holders of risky assets and use a dynamic model framework that assumes a partial adjustment of the ratio of risky assets, reducing the gap between their optimal and present ratios (Figure 5).

Figure 5: Analytical framework

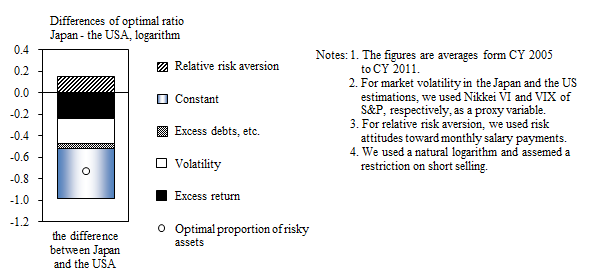

The results indicate that the factor of the classical theory performs an important role in determining the optimal ratio of risky assets (Ito et al. 2017 [PDF 833KB]). Moreover, it also indicates that differences in the expected value of excess returns on risky assets and market volatility subsequently influence differences in portfolio selection between Japanese and US households. In addition, factors other than the explanatory variables captured by the constant term in our model also have a large effect (Figure 6).

Figure 6: Breakdown of the differences in the optimal ratio of risky assets between Japanese and US risky asset holders

Next, we report results elucidating the background of a few households holding risky assets in Japan. Specifically, we expand the scope of analysis to all households in Japan and the USA and investigate the influence of explanatory variables, such as the factors of the classical theory, liquidity constraints, precautionary saving motives, and entry costs, to determine the participation rate. Our results indicate that the factors of the classical theory, liquidity constraints, and precautionary saving motives significantly affect participation rates both for Japanese and US households (Table 2). In addition, we confirm that financial literacy, especially regarding investment diversification and bond prices, is strongly related to the possession of risky assets. For instance, households who correctly answered the question about bond prices had approximately a 20% higher probability of holding risky assets.

Table 2: Results of testing households' participation rate in Japan and the USA

| Explanatory variable | Marginal effects | ||

|---|---|---|---|

| The factor of excess return, volatility, and relative risk aversion (%) | 0.4 | *** | |

| Liquidity Constraints | Excess debts (0,1) | -9.5 | ** |

| Loan rejection (0,1) | -27.1 | *** | |

| Precautionary Saving | Concerns about unemployment (0,1) | -3.1 | |

| Concerns about later life (0-2) | -12.3 | *** | |

| Entry Costs | Compound interest (0,1) | -2.1 | |

| Inflation (0,1) | 13.6 | *** | |

| Investment diversification (0,1) | 18.2 | *** | |

| Bond prices (0,1) | 21.2 | *** | |

| Constant | Japan dummy (0,1) | -13.8 | *** |

Notes:

- *** and ** denote significance at the 1% and 5% levels, respectively.

- Marginal effects represent the range of change (%) in risky asset holding probability when the explanatory variable increases by one unit.

- Figures for financial literacy are dummy variables that take the value of unity for households who correctly answered and zero otherwise.

- For concerns about later life, we apply two to households who selected "Particularly True" to the question regarding concerns about life situations in their old age, one to households who selected "True," and zero otherwise.

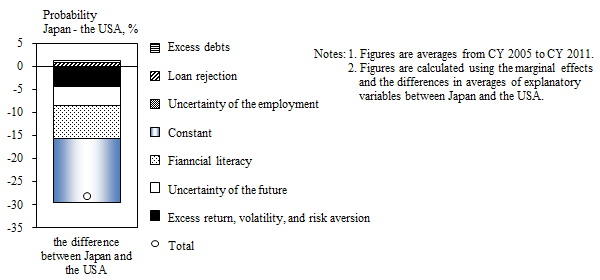

As a consequence, we break down the probability difference of holding risky assets between Japanese and US households by using the estimation results (Figure 7). These indicate that while the factors of the classical theory and concerns about later life affect the probability of holding risky assets, the major difference is explained by financial literacy and a factor captured by the constant term (structural factors in Japan and the USA). The large influence of the constant term, similar to the analysis regarding households holding risky assets, is shown in Figure 6. While it is difficult to specify the factor of the constant term, the difference in institutional aspects of portfolio selection between Japan and the USA may be one factor, not explicitly considered in our model. During the estimation period (from 2005 to 2011), for instance, many US households invested in risky assets through a defined contribution pension system, such as a 401(k), whereas Japanese households invested only minimally in risky assets.4 In addition, structural factors, such as differences in values and cultures, may exert some influence.

- 4In this regard, the target of individual-type Defined Contribution Pension plans (iDeCo) in Japan has been greatly expanded in 2017.

Figure 7: Breakdown of the differences in the probability of holding risky assets between Japanese and US households

Although the differences in portfolio selection between Japan and the USA can be explained to some extent by the risk-return relationship in the markets and by concerns about later life, other factors are also indispensable, particularly financial literacy. In addition, structural factors such as differences in institutional aspects of portfolio selection in Japan and the USA could conceivably exert an important influence.

Conclusion

Based on these results, it is also necessary for the improvement of Japanese household investment circumstances to further improve institutional aspects and enrich the dissemination of financial education, in addition to improving the risk-return relationships in the market and mitigating various household constraints such as concerns about the future. In this regard, steady efforts to improve financial literacy have been undertaken, alongside enhancement of institutions such as NISA (individual savings accounts in Japan) and defined contribution pension systems. These measures are expected to encourage households to invest in more risky assets in the future.

Finally, we indicate future research possibilities. In testing the framework of this study, we do not analyze the asset selection mechanism of real assets and the long-term impact of changes in demographics, such as aging, on a household's portfolio selection. The acquisition of real assets and a household's lifecycle are important, decisive factors in portfolio selection. Elucidating their influence would be a fruitful exercise for future research. Moreover, it is also important to clarify the underlying mechanisms that influence a household's portfolio selection behavior, such as the expected return.

Reference

- Aoki, K., A. Michaelides, and K. Nikolov (2016), "Household Portfolios in a Secular Stagnation World: Evidence from Japan [PDF 970KB] ," Bank of Japan Working Paper Series, No.16-E-4.

- Barsky, R. B., F. T. Juster, M. S. Kimball, and M. D. Shapiro (1997), "Preference Parameters and Behavioral Heterogeneity: An Experimental Approach in the Health and Retirement Study," Quarterly Journal of Economics, 112(2), pp. 537-579.

- Ito, Yuichiro, Yasutaka Takizuka, and Shigeaki Fujiwara (2017), "Portfolio Selection by Households: An Empirical analysis Using Dynamic Panel Data Models [PDF 833KB]," Bank of Japan Working Papers, No. 17-E-6.

- Iwaisako, T., A. Ono, S. Saito, and H. Tokuda (2015) "Residential Property and Household Stock Holdings: Evidence from Japanese Micro Data," The Economic Review (In Japanese), 66(3), 242-264.

- Klapper, L., A. Lusardi, and P. Van Oudheusden (2015), "Financial Literacy Around the World: Insights from the Standard & Poor's Ratings Services Global Financial Literacy Survey," Report, Global Financial Literacy Excellence Center, The George Washington University School of Business.

- Mankiw, N. G., and S. P. Zeldes (1991), "The Consumption of Stockholders and Nonstockholders," Journal of Financial Economics, 29(1), pp. 97-112.

- Merton, R. C. (1969), "Lifetime Portfolio Selection under Uncertainty: The Continuous-Time Case," Review of Economics and Statistics, 51(3), pp. 247-257.

- Nakajo, M., J. Shino, and K. Imakubo (2017), "Behavioral Characteristics Affecting Household Portfolio Selection in Japan [PDF 190KB]," Bank of Japan Review Series, No. 17-E-3.

- Samuelson, P. A. (1969), "Lifetime Portfolio Selection by Dynamic Stochastic Programming," Review of Economics and Statistics, 51(3), pp. 239-246.

Notice

The views expressed herein are those of the authors and do not necessarily reflect those of the Bank of Japan.