Financial System Report (October 2022)

October 21, 2022

Bank of Japan

Motivations behind the October 2022 issue

This issue of the Report focuses on financial institutions' domestic and foreign lending and securities investment and assesses potential vulnerabilities in Japan's financial system by analyzing them from the following two perspectives.

First, the Report examines potential credit risk posed to financial institutions with regard to additional stress. In Japan, while demand for additional loans due to the pandemic has subsided on the whole, firms' financing stance has remained cautious. Outside Japan, as major banks have strived to expand their international business, loans to highly leveraged firms have been increasing. The recent rises in energy and raw material prices and foreign interest rates could put additional stress on these borrower firms.

Second, the Report examines the impact of the rise in foreign interest rates on financial institutions' foreign net interest income and valuation gains/losses on securities holdings. Many financial institutions have aimed at improving their profitability by enhancing securities investment. In the past few years, in addition to yen-denominated bonds, financial institutions have increased investments in foreign bonds and foreign bond investment trusts. For these institutions, the decline in interest and dividends on securities and the decrease in room for realizing gains could reduce their loss-absorbing capacity.

Executive summary: Stability assessment of Japan's financial system*

Japan's financial system has been maintaining stability on the whole. Japanese financial institutions have kept sufficient capital and liquidity even under various types of stress since the outbreak of COVID-19, including supply constraints and rises in energy and raw material prices under the normalization of economic activity and the materialization of geopolitical risks. However, the period of stress may be prolonged further as policy rate hikes by central banks are continued and concerns about a slowdown in foreign economies are spreading. Financial and capital markets have continued to be nervous.

From a long-term perspective, if financial institutions' core profitability were to stagnate, financial intermediation could be impaired due to a decline in loss-absorbing capacity, or vulnerabilities in the financial system could increase through excessive risk-taking. To ensure the stability of Japan's financial system, it is necessary to examine these contraction and overheating risks in the financial system and address potential vulnerabilities appropriately.

The current phase of the financial cycle

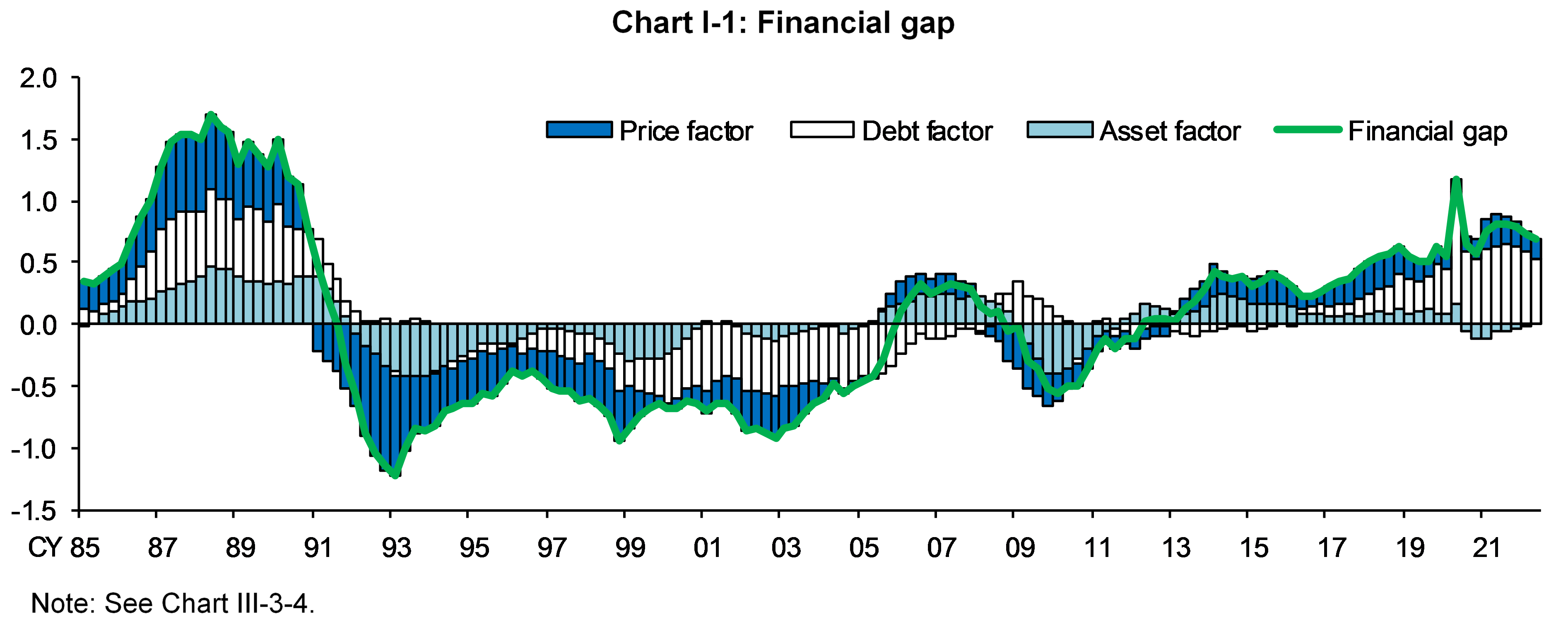

The financial gap, which captures the financial cycle, has been widening, albeit at a moderate pace, against the background of smooth functioning of financial intermediation. Almost a decade has passed in the current expansionary phase of the cycle, largely due to an increase in private debt (the "debt factor") (Chart I-1). In the current phase, however, the contribution of an increase in real investment (the "asset factor") and a rise in asset prices (the "price factor") has been limited. No major financial imbalances -- such as an increase in leverage, driven by the accumulation of private debt and active investment, together with an increase in asset prices -- can be observed.

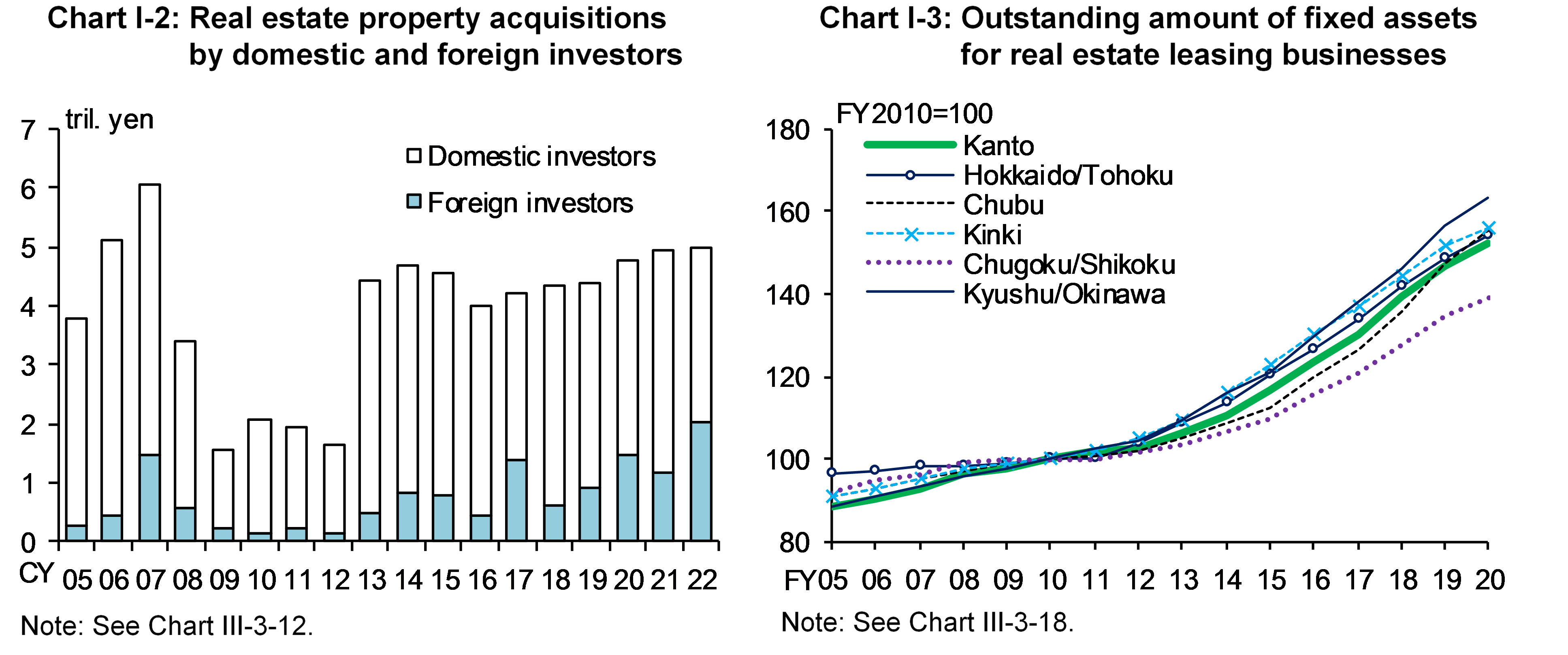

About half of the increase in total credit in the past decade can be explained by increases in household loans and real estate loans. Real estate loans by major banks have kept rising, particularly those to real estate investment funds (Chart I-2). This is because foreign investors have continued to engage in transactions at high prices against the background of relatively stable profitability in Japan's real estate market. Moreover, real estate loans by regional financial institutions have also continued to increase in parallel with investment in fixed assets by real estate leasing businesses (Chart I-3). In the real estate market, office rent has started to decline and the financial leverage of real estate leasing businesses has been increasing. Against this backdrop, attention should be given to the investment behavior of foreign investors and real estate leasing businesses.

Domestic firms' financial condition under prolonged stress

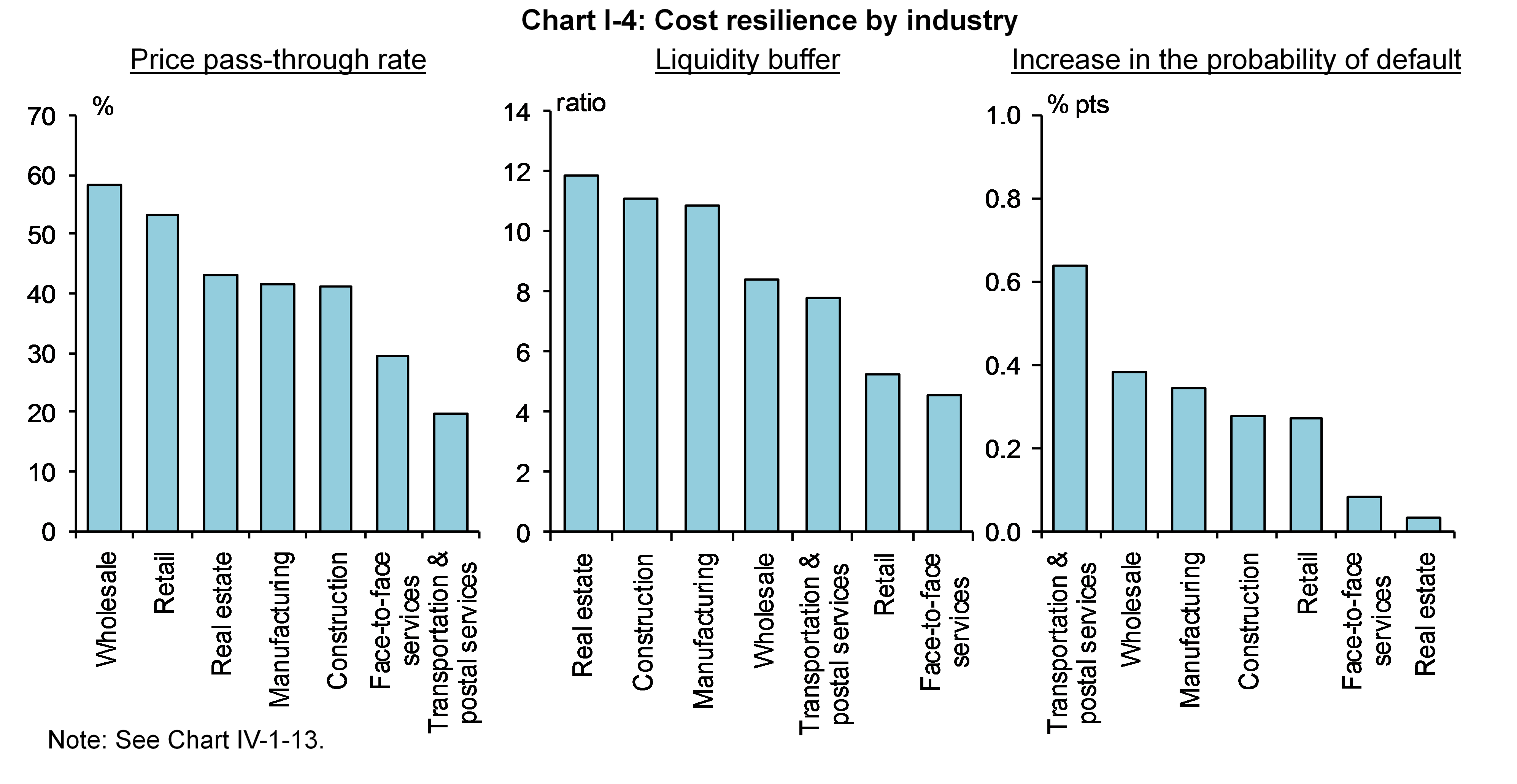

Even amid the prolonged period of stress, many firms have kept ample liquidity buffers. This is partly why defaults have been restrained at historically low levels. However, firms have faced higher raw material input costs due to the rise in import prices. For some of these firms that have had difficulty passing them on to sales prices, the probability of default (PD) could rise significantly. According to the analysis, the PD is likely to increase for (1) firms for which variable costs are sensitive to import prices due to their heavy dependence on imports, (2) firms with limited bargaining power in price negotiations with their counterparties, and (3) firms heavily affected by the pandemic and with resulting low liquidity buffers (Chart I-4).

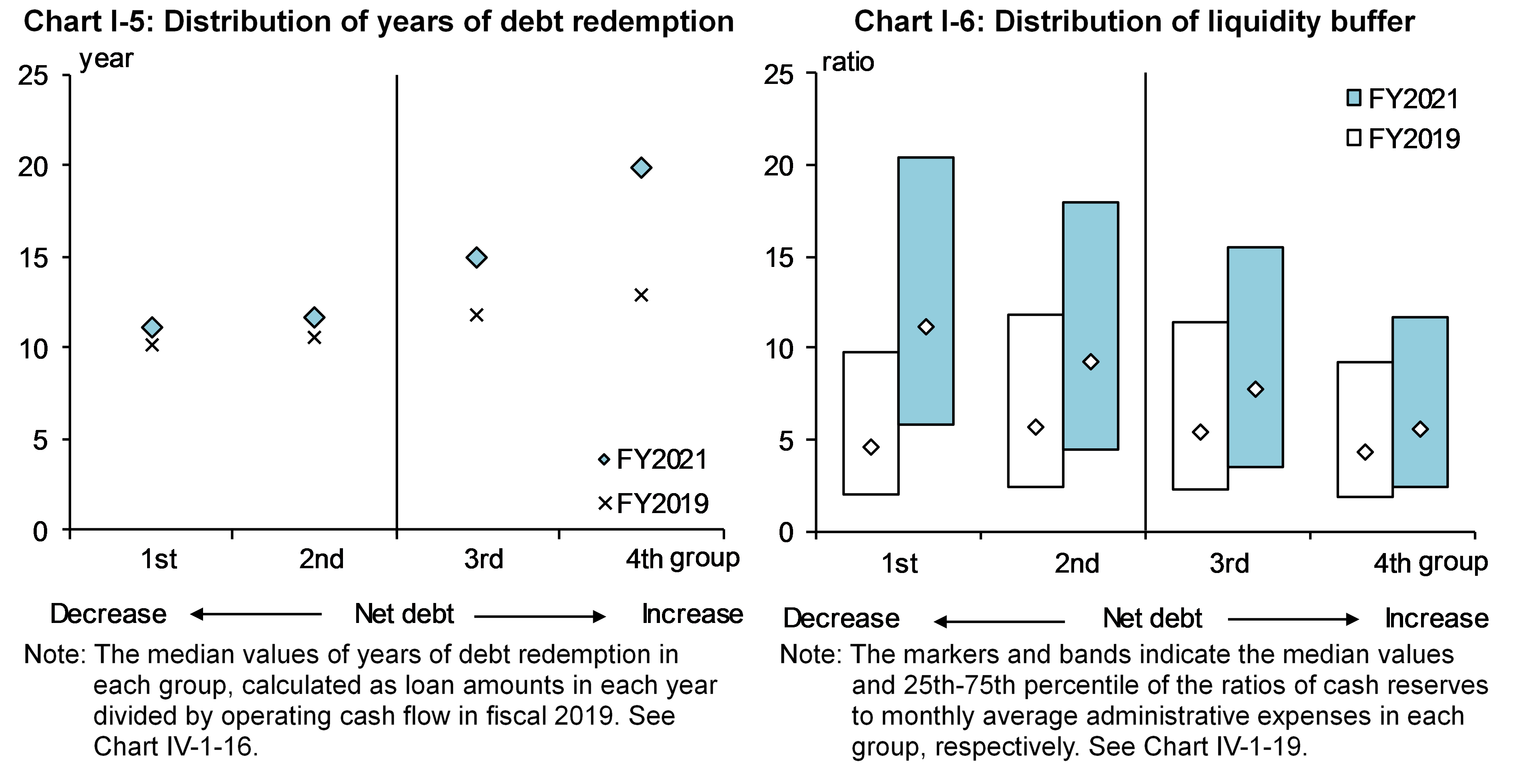

Pandemic-related loans, including effectively interest-free loans, have strongly supported firms' finances during the pandemic. For many of these loans, repayment has already started. Small and medium-sized enterprises (SMEs) for which net debt has increased since the outbreak of the pandemic tend to have loans with longer durations (Chart I-5). They also tend to hold a lower liquidity buffer and are less resilient to additional stress (Chart I-6). Amid the prolonged period of stress, financial institutions are expected to continue to encourage firms to improve their operating cash flow.

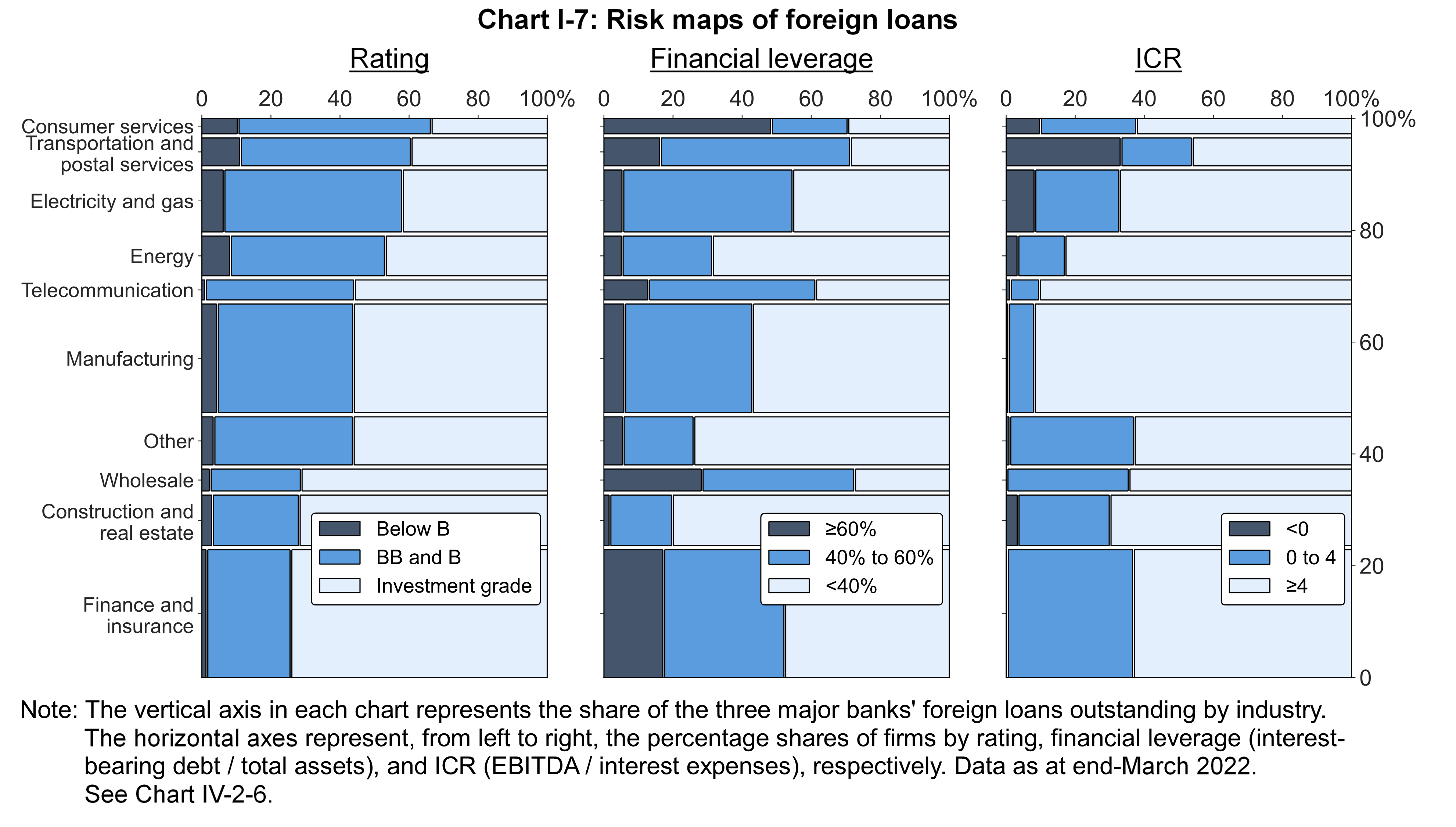

Interest rate sensitivity of foreign loans

The foreign loans maintain a high level of investment grade ratio. With foreign interest rates rising quickly, however, there is a risk that the creditworthiness of highly leveraged firms could deteriorate. A risk map visualizes relationships between the outstanding amount of foreign loans by industry, the borrower credit rating, and the borrower financial indicators (Chart I-7). It shows that even industries with a high share of investment grade firms have quite a few firms with high leverage and a low interest coverage ratio. Moreover, the recent growth in leveraged loans has been pushing up the shares of non-investment grade firms and highly leveraged firms in foreign loans.

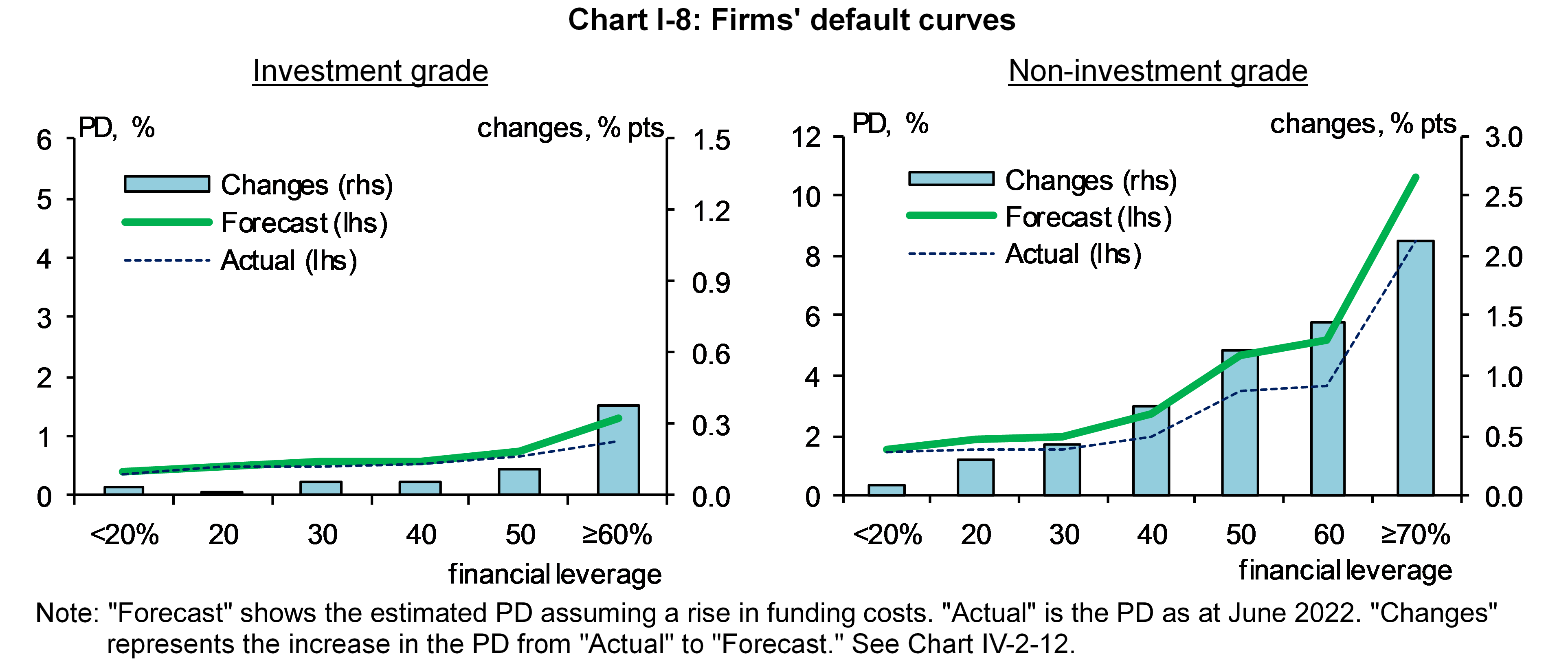

As shown in the risk map, the foreign loan portfolios have a somewhat high percentage of highly leveraged firms, which are likely to be sensitive to interest rate rises. To quantify the sensitivity, an increase in firms' PD in response to an increase in funding costs is estimated. The result shows that the response of the PD tends to be more amplified, the higher firms' financial leverage (Chart I-8). It also shows that the default curve as a result of a rise in firms' funding costs shifts upward and its slope becomes steeper as firms' financial leverage increases. Financial institutions need to refine their credit risk management with regard to highly leveraged firms.

Financial institutions' resilience to foreign interest rate rises

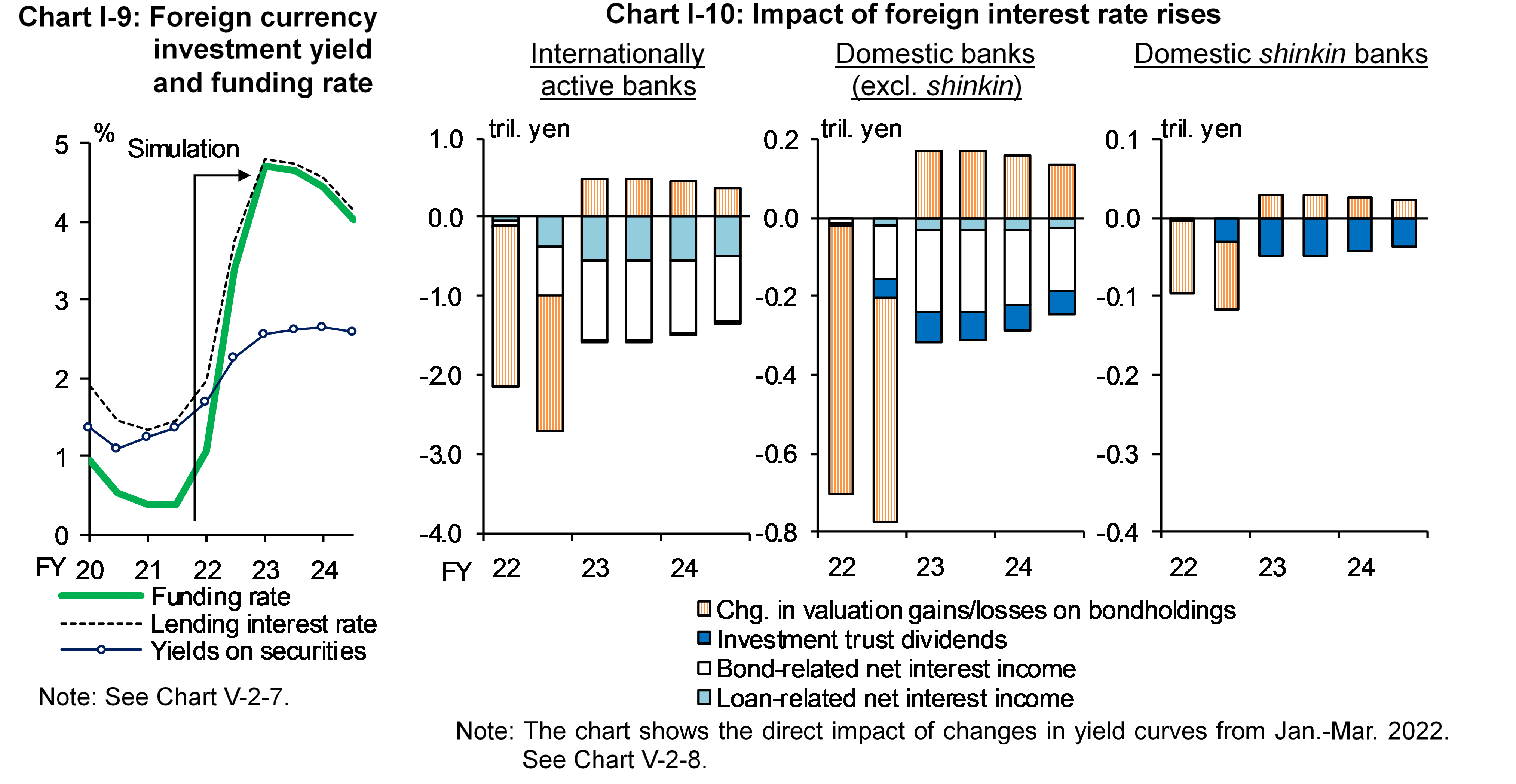

Financial institutions' valuation losses on securities have increased recently, and such losses could increase further depending on future developments in interest rates. In the short term, the rising cost of foreign currency funding could result in a negative spread between investment yields and funding rates of foreign currency. Among financial institutions that had increased their risk-taking on foreign currency interest rate to improve their profitability, there are some that are increasingly dependent on profits from foreign currency interest and dividends. Thus, attention should be given to a decline in the loss-absorbing capacity of such financial institutions in the event of deterioration in gains from securities investment.

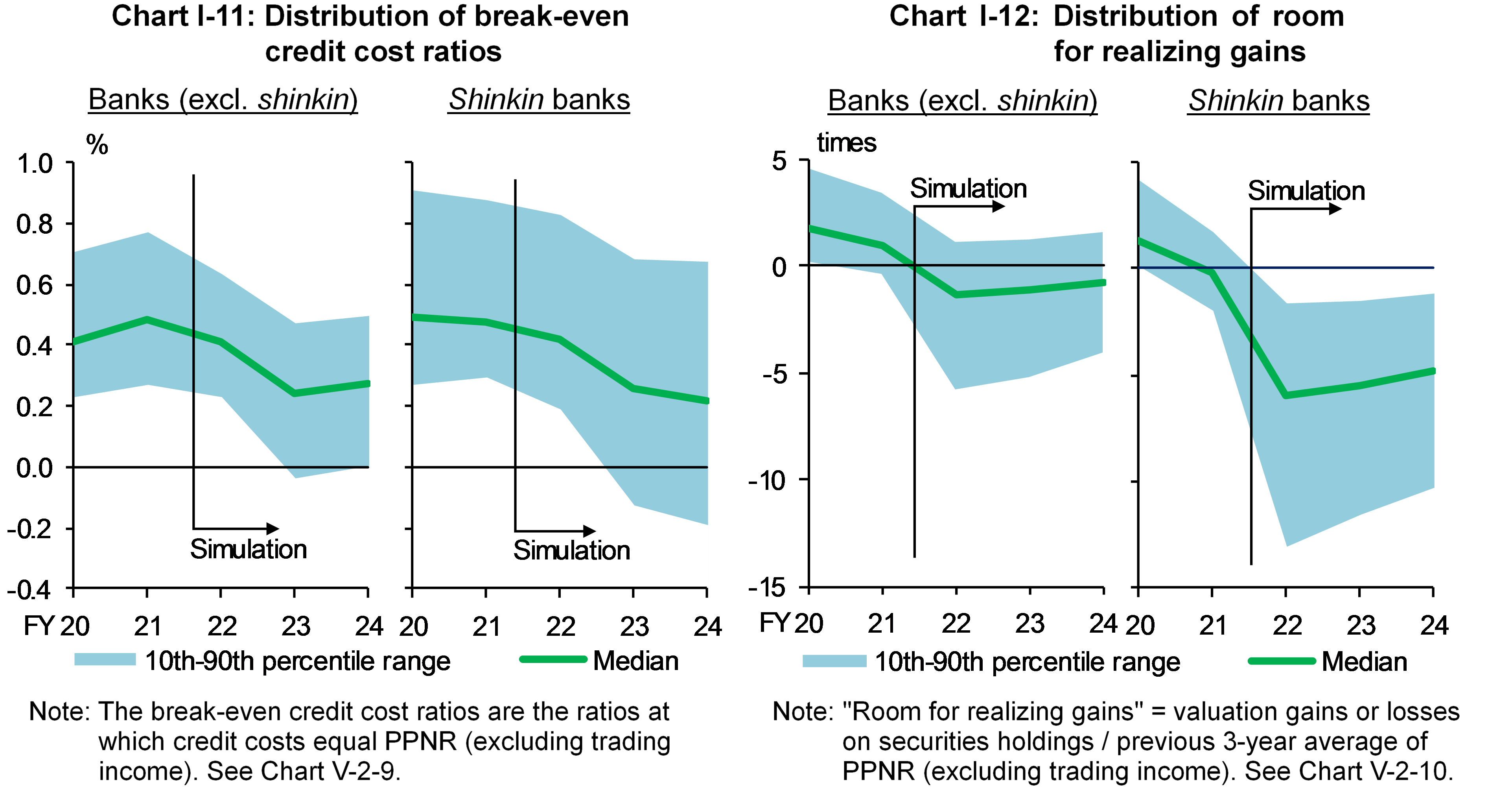

The results of the macro stress testing indicate that Japanese financial institutions on the whole are resilient to stress events such as a substantially inverted yield curve in foreign markets. However, in such a stress event, foreign lending margins are squeezed substantially, and margins on securities investment turn negative (Chart I-9). In that case, the following factors are expected to contribute significantly to the decrease in foreign net interest income: the fall in loan-related and bond-related net interest income for internationally active banks, the fall in bond-related net interest income and investment trust dividends for domestic banks excluding shinkin banks, and the fall in investment trust dividends for domestic shinkin banks (Chart I-10). Moreover, the break-even credit cost ratios, which represent profit buffers, are expected to decline as a whole (Chart I-11).

Since valuation gains/losses on bondholdings would deteriorate in the initial phase of interest rate rises, financial institutions' room for realizing gains could decline considerably (Charts I-10 and I-12). Such financial institutions would have difficulty in engaging in additional risk-taking, and their profitability would become more likely to decline. The functioning of financial intermediation could be impaired for some financial institutions.

The Bank of Japan will promote financial institutions' initiatives to address these potential vulnerabilities through on-site examinations and off-site monitoring. It will continue to closely monitor the impact of various risk-taking moves by financial institutions on the financial system from a macroprudential perspective.

- See the Report for more details on the analyses as well as notes and sources of the charts.

Notice

This Report basically uses data available as at end-September 2022.

Please contact the Financial System and Bank Examination Department at the e-mail address below to request permission in advance when reproducing or copying the contents of this Report for commercial purposes.

Please credit the source when quoting, reproducing, or copying the contents of this Report for non-commercial purposes.

With regard to economic and financial variables of each stress scenario in the macro stress testing, please see the scenario tables [XLSX 37KB] .