Financial System Report (April 2026)

April 21, 2026

Bank of Japan

Motivations behind the April 2026 issue

In global and domestic financial markets, crude oil prices surged and asset prices and long-term interest rates fluctuated significantly in the wake of increased tension over the situation in the Middle East since the end of February. In addition to the future course of the situation in the Middle East, the performance of major foreign high-tech stocks, and the loan and investment activities of foreign non-bank financial intermediaries (NBFIs) have also been drawing close attention. This Report assesses the stability of the financial system under such significant changes in the external environment.

With regard to foreign NBFIs, such as hedge funds, which are increasing their presence both domestically and globally, this Report examines the characteristics of their global investment activities and assesses the potential impact on Japanese financial markets of shocks originating in foreign markets. It also examines developments in private funds.

In addition, while no major imbalances have been seen in the domestic financial cycle, Japanese banks have increased their lending, both domestically and globally, as they actively respond to strong loan demand. Specifically, the growth in real estate-related lending has accelerated as the upward trend in real estate prices continues, and there has been an increase in loans to foreign investment funds, which have unique risk characteristics. This Report examines banks' lending stance and the risks associated with such loan exposures.

Corporate bankruptcies and corporate loan defaults, housing loan delinquency rates, and banks' resilience to rising interest rates exhibit no significant changes at present, amid the changing environment regarding interest rates. With that being said, this Report also examines the key points that warrant attention under the continued increase in interest rates and their impact on banks' balance sheets.

The macro stress test assesses the adequacy of banks' capital by using stress scenarios that were constructed following the increased tensions in the Middle East.

Executive summary: Stability assessment of Japan's financial system*

Japan's financial system has been maintaining stability on the whole.

In the loan market, financial intermediation has continued to function smoothly as firms' demand for loans has continued to rise and banks' lending stance has remained active. Under such circumstances, no major financial imbalances have been seen in current financial activities.

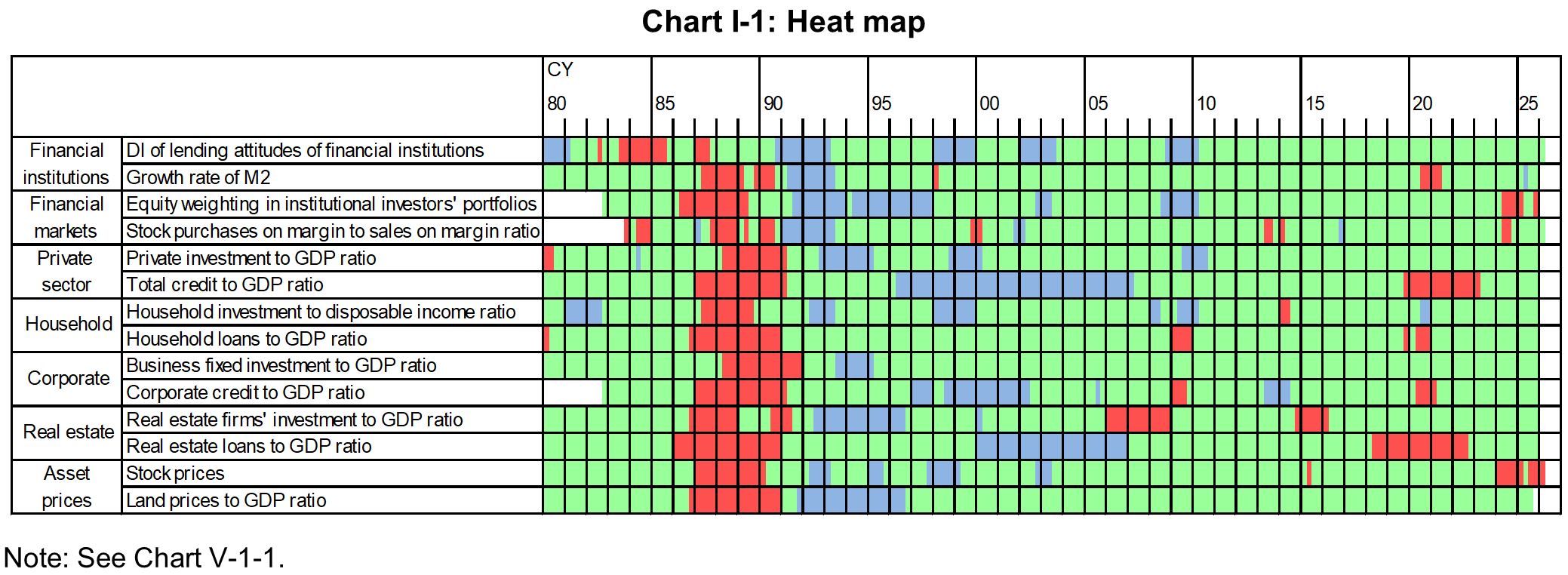

Japanese banks have sufficient capital bases and stable funding bases to withstand various stress situations, specifically including (1) stress equivalent to the global financial crisis that would cause major corrections in financial markets and the real economy at home and abroad; and (2) a compound stress of the materialization of geopolitical risks such as a rise in crude oil prices, together with shrinking expectations about future prospects for AI, and a substantial rise in interest rates, all happening simultaneously. However, it is necessary to carefully monitor the impact on the financial system, which could materialize through various channels, of developments in the economic policy formulation in each jurisdiction, geopolitical risks particularly regarding the situation in the Middle East, and activities of the foreign non-bank financial intermediary (NBFI) sector. From a long-term perspective, if structural factors such as a decline in firms' loan demand reflecting the shrinking population and other factors persist, banks' profitability and loss-absorbing capacity could decline, depending on the supply and demand balance in the loan market, and this could lead to a contraction of financial intermediation activities or an overheating, such as excessive search for yield. From the perspective of maintaining stability in Japan's financial system, close attention is warranted on future developments in the system, while examining both overheating and contraction risks (Chart I-1).

Corporate bankruptcies and defaults

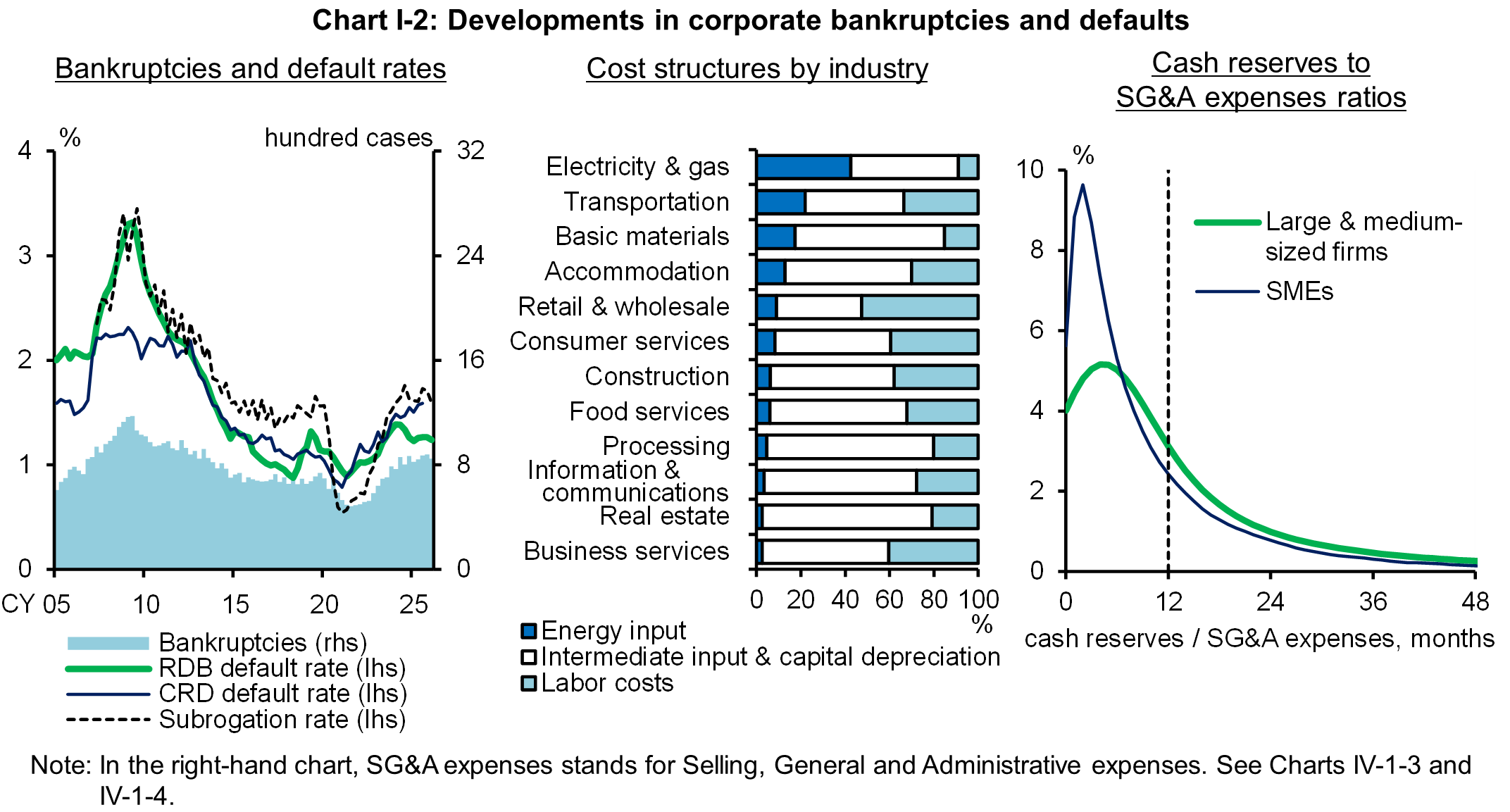

Corporate bankruptcies and default rates have been more or less unchanged, albeit with fluctuations (left panel of Chart I-2). Corporate profits have been improving on the whole amid the continuing moderate economic recovery, and the share of firms making operating losses with negative net worth or those making operating losses, which increased during the pandemic, has been falling. However, attention should continue to be paid to the point that labor costs and past increases in raw material prices are imposing an additional burden, particularly on financially vulnerable firms.

Moreover, crude oil prices surged in the wake of increased tension over the situation in the Middle East that happened at the end of February. Depending on the future course of the situation in the Middle East, firms' commodity procurement costs could be elevated, and there is a risk that production activities face downward pressure through the effects on supply chains. Under these circumstances, it remains necessary to pay close attention to the possibility that this could have an impact on firms' financial positions and their cash flow management (middle and right panels of Chart I-2).

Developments in asset prices

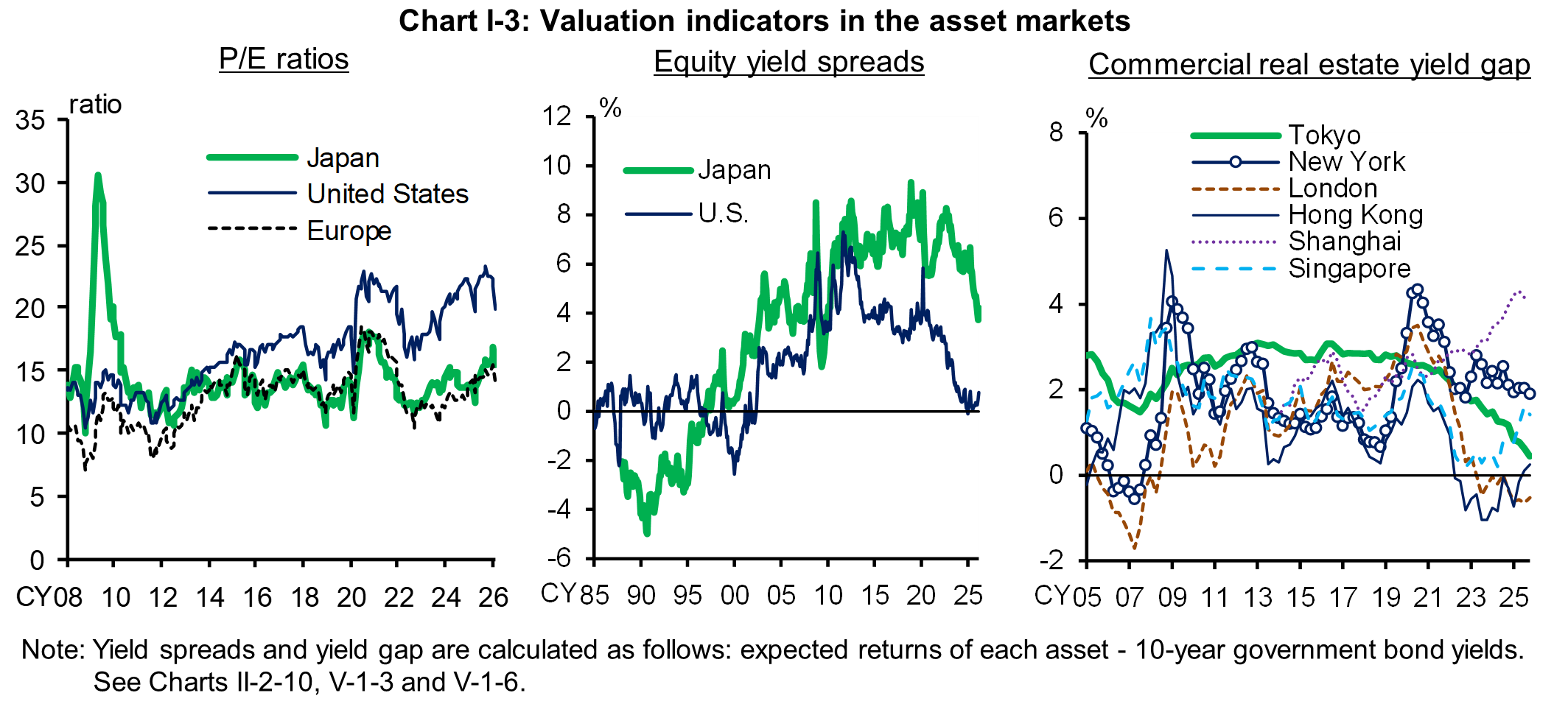

Regarding the stock market, the stock prices indicator has continued to deviate upward from its trend, as shown by "red" in the heat map, although stock prices have declined in the wake of increased tension over the situation in the Middle East since the end of February (Chart I-1). In terms of stock valuations as of the end of March, price-earnings (P/E) ratios have remained broadly around their average levels since 2008, reflecting an increase in expected earnings per share (EPS), which is the denominator (left panel of Chart I-3). Risk premiums indicated by the equity yield spreads, i.e., the difference between expected equity yields and 10-year Japanese government bond (JGB) yields, have declined somewhat amid rising interest rates (middle panel of Chart I-3). Given that there are concerns about geopolitical risks, particularly regarding the situation in Middle East, and adjustment risks in foreign high-tech-related stocks, and that Japanese banks have a certain amount of market risk associated with stockholdings, close attention should continue to be paid to developments in risky asset prices, including stock prices.

Real estate prices have been rising, particularly in major metropolitan areas. Higher construction costs and supply constraints due to labor shortages have contributed to the rise in real estate prices. In addition, robust property demand supported by a moderately recovering economy, coupled with demand for investments, including condominium transactions and commercial real estate purchases by foreign investors, have also likely contributed to this trend. While rents have been rising, the yield gap, an indicator of the real estate risk premium, has continued to decline (right panel of Chart I-3). Developments in real estate markets continue to warrant attention.

Developments in bank lending

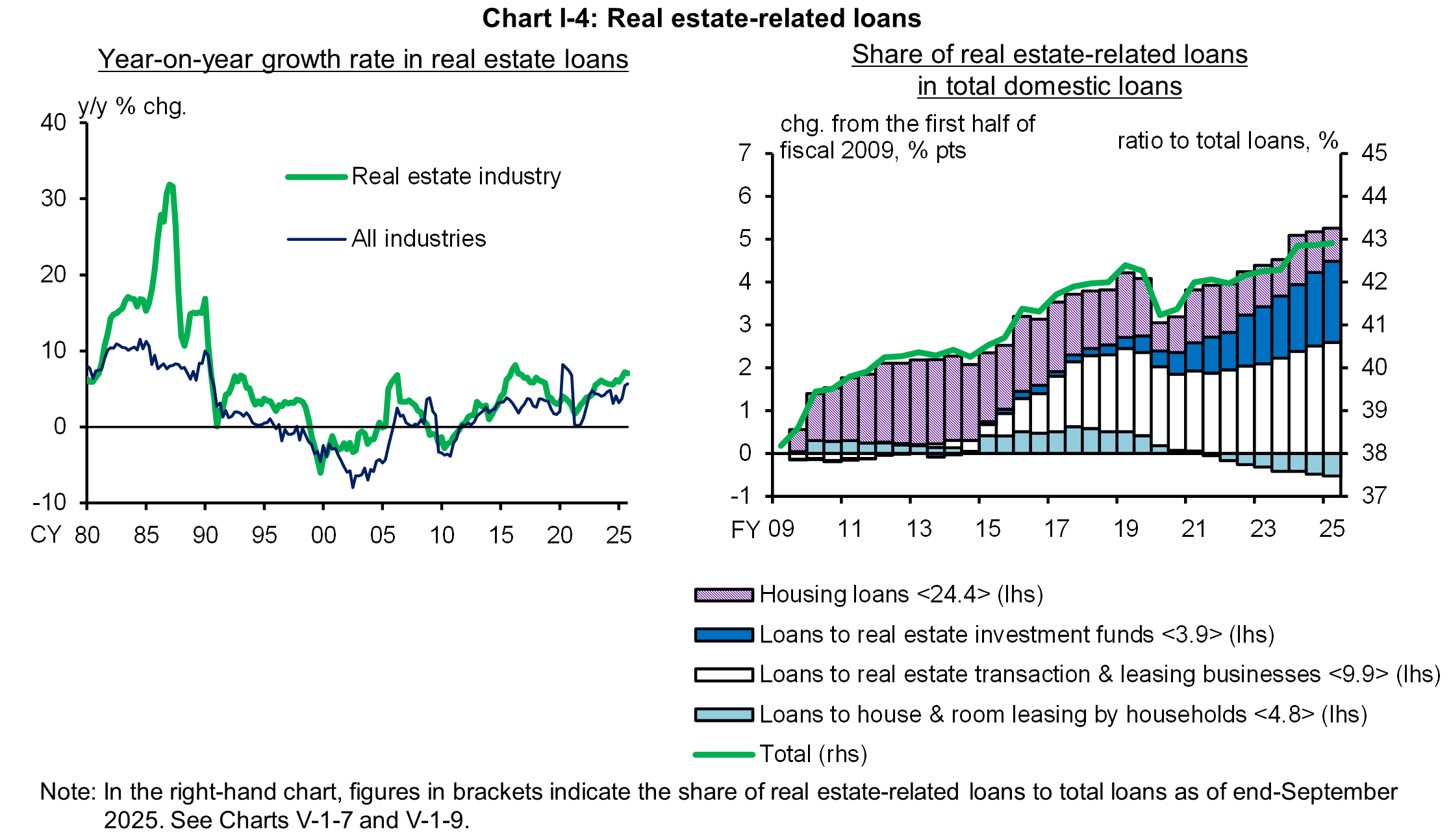

The growth of bank lending has increased somewhat recently. Real estate-related lending in particular has continued to grow at a faster pace than overall lending, reflecting the sustained robust funding demand from the real estate industry (left panel of Chart I-4). Banks appear to be meeting the firm demand from the real estate industry while remaining prudent in their credit management. It should be noted, however, that in recent years, the share of real estate-related lending in total lending has been on an uptrend, and that, within this loan segment, there is a gradual shift in lending to real estate businesses (excluding house and room leasing by households) and to real estate funds (right panel of Chart I-4). Banks need to manage credit risks taking into account the risk profiles of borrowers and changes in their composition, and also paying due attention to the risk of fluctuations in real estate prices and to the possibility that the transmission channels of stress may differ from those in the past.

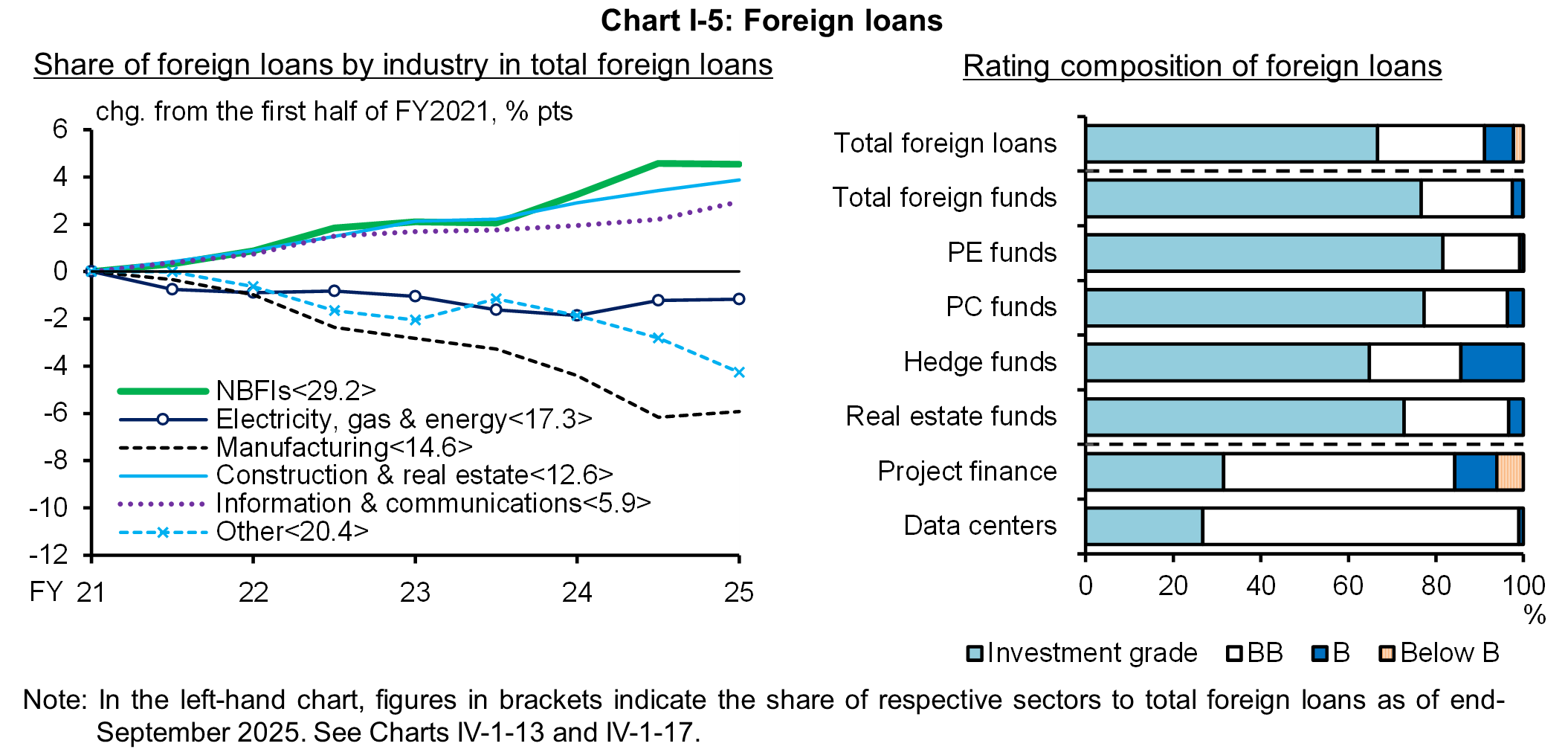

In banks' overseas lending, the share of loans to the NBFI sector, construction and real estate, and the information and communications sector has increased recently (left panel of Chart I-5). The share of loans to foreign investment funds and loans to data centers in their total overseas lending is not large, and banks at present rarely classify these loans as "below B" (right panel of Chart I-5). However, creditworthiness could change significantly as a result of changes in the business environment, such as technological innovations and shifts in valuations of the underlying assets that form the source of repayment for such loans. In addition, a wide range of loans to the above sectors could potentially be affected simultaneously through similarities in the underlying assets. With regard to activities related to private credit (PC), recent cases of investor redemptions, particularly by retail investors, from certain PC funds have attracted attention, and future developments warrant careful attention. Banks should continue to pay close attention to the quality management of their portfolios when undertaking credit activities in such areas of focus in lending activities.

Global investment activities of the foreign NBFI sector

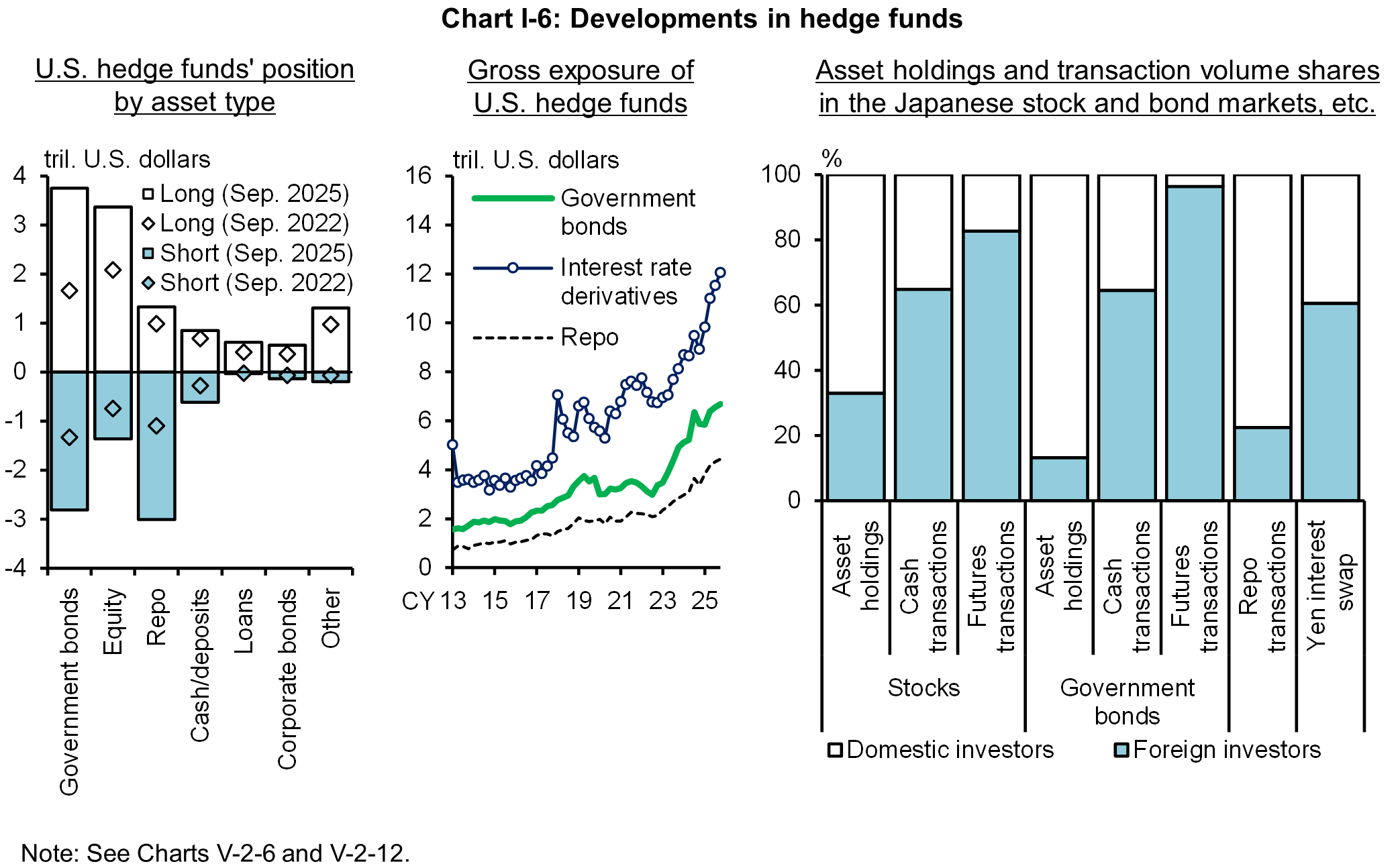

Amid the growing interconnectedness of Japan's financial system with the foreign NBFI sector, it is necessary that banks manage their risks associated with securities holdings while paying attention to the possibility of investment activities by the foreign NBFI sector causing stress in domestic financial markets.

Developments in hedge funds operating in the United States reveal a continued expansion of both long and short positions in bond markets, particularly in sovereign bonds of major countries, indicating that the presence of such funds has further increased globally (left and middle panels of Chart I-6). Foreign hedge funds have been trading JGBs combined with repos and derivatives such as interest rate swaps, resulting in increased leverage, and as such they have been increasing their presence in Japan's bond market (right panel of Chart I-6). Close attention is needed to the possibility that, if foreign hedge funds were to unwind positions globally in an event of stress, the impact could spread to Japan's bond market through, for instance, a decline in market liquidity.

Banks' profits and loss-absorbing capacity amid rising interest rates

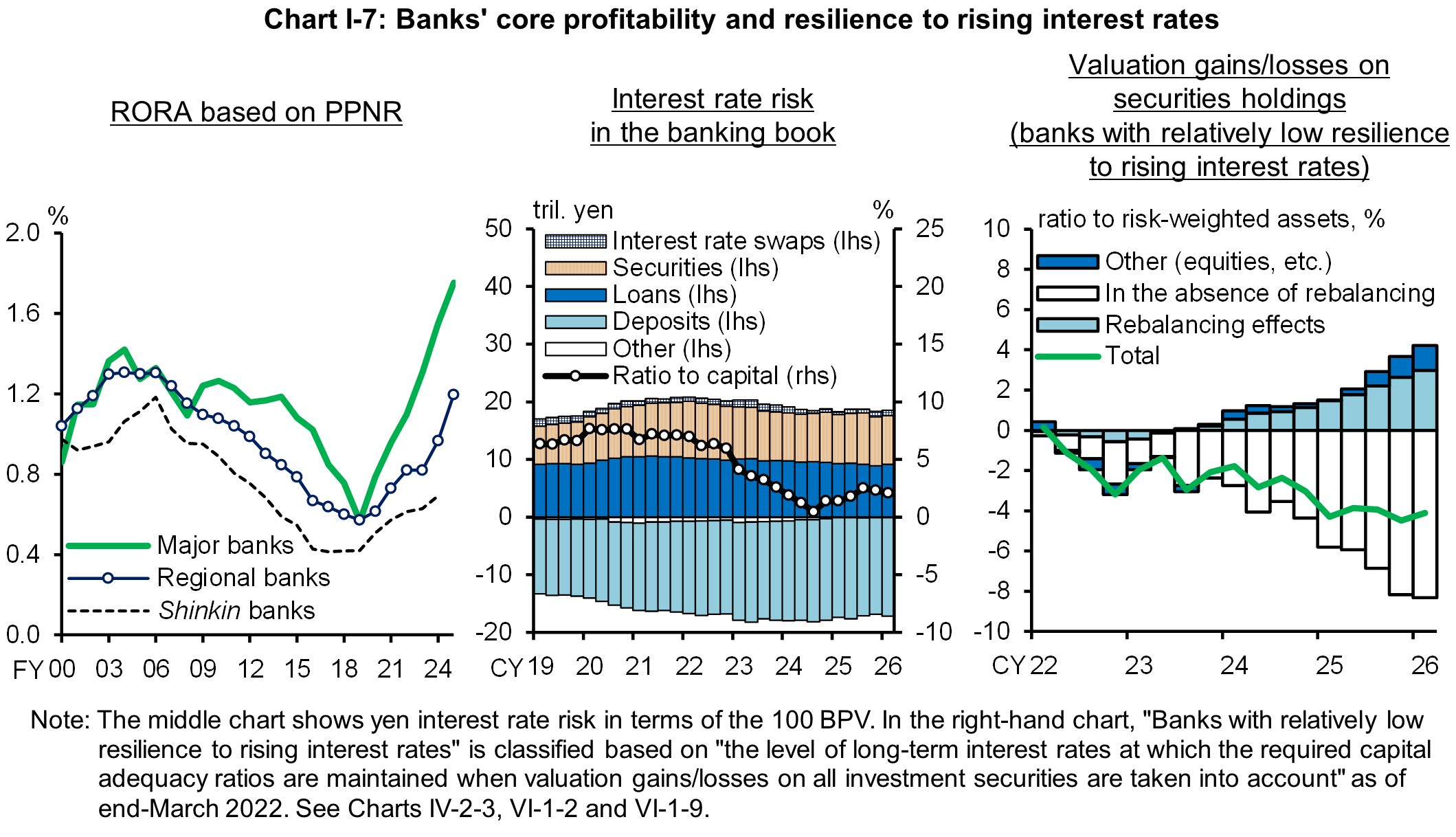

Banks' pre-provision net revenue (PPNR), which shows banks' core profitability, has continued to improve owing to limited losses on credit costs, etc., with the Japanese economy exhibiting ongoing moderate recovery, past improvement in overhead ratios, and rising yen interest rates (left panel of Chart I-7). That said, increases in non-personnel expenses and in personnel expenses have continued, and downward pressure remains on banks' profitability from structural factors such as a decline in domestic loan demand due to the shrinking population and the falling number of domestic firms. These developments warrant careful attention.

Turning to banks' resilience to rising interest rates, yen interest rate risk in the banking book (IRRBB), measured as the 100 BPV relative to banks' capital, has remained low (middle panel of Chart I-7). Overall, banks have sufficient loss-absorbing capacity. Although valuation losses on securities holdings, particularly yen-denominated bonds, have worsened due to the recent rise in interest rates, net valuation losses on securities holdings of banks even with relatively low resilience to interest rate rises have still remained at around the same level as in March 2025, as banks have continued to decrease their outstanding amount of yen-denominated bondholdings and to shorten their durations (right panel of Chart I-7). Banks need to continue managing their portfolios appropriately by taking into account various scenarios regarding market fluctuations and the impact of future changes in the composition of their balance sheets.

The Bank will promote financial institutions' initiatives to address these potential vulnerabilities through on-site examinations and off-site monitoring. From a macroprudential perspective, it will continue to closely monitor the impact on the financial system of various risk-taking activities by financial institutions.

- See the Report for more details on the analyses as well as notes and sources of the charts.

Notice

This Report basically uses data available as of end-March 2026.

Please contact the Financial System and Bank Examination Department at the e-mail address below to request permission in advance when reproducing or copying the contents of this Report for commercial purposes.

Please credit the source when quoting, reproducing, or copying the contents of this Report for non-commercial purposes.

With regard to economic and financial variables of each stress scenario in the macro stress testing, please see the scenario tables [XLSX 21KB].

Inquiries

Financial System Research Division,

Financial System and Bank Examination Department

E-mail : post.bsd1@boj.or.jp