Structure of P2P lending and investor protection: Analyses based on an international comparison of legal arrangements

Atsushi Samitsu (Bank of Japan)

Research LAB No17-E-6, October 23, 2017

Keywords: P2P lending; Financial intermediation; Banks; Systemic risk; Investor protection; FinTech

JEL Classification: K22

Contact: atsushi.samitsu@boj.or.jp

Abstract

P2P lending is direct lending between lenders and borrowers online without using traditional financial intermediaries such as banks. There has been a rapid increase in the amount of outstanding loans in P2P lending in recent years, mainly in the UK, the US, and China, since a major P2P lending platform in the UK was launched in 2005. In this paper, the structure of P2P lending and its characteristics are analysed using banks as a reference point. This paper also highlights the fact that the legal arrangements in P2P lending vary from country to country and those differences could affect the degree of investor protection. Samitsu (2017) explains that under the current legal arrangement in Japan, investors assume the credit risk of P2P lending platforms, and proposes utilising schemes such as specific purpose companies and specific trust companies to strengthen investor protection.

Introduction

In recent years, FinTech - technologically-enabled financial innovation that could result in new business models, applications, processes or products with an associated material effect on financial markets and institutions and the provision of financial services (Carney, 2017) - has attracted considerable attention. One prominent example of a FinTech business is P2P lending. There has been a rapid increase in the amount of outstanding loans in P2P lending in the UK since the launch in 2005 of a major P2P lending platform. Similar developments have also been observed in the US and China.

There are two aspects of P2P lending that have helped its growth. First, the cost of conducting business is low because P2P lending platforms have little need for a physical presence or human resources to operate. In addition, while banking regulations and the supervision of banking activities have become increasingly stringent since the global financial crisis, the activities of P2P lending platforms are not subject to those regulations.

P2P lending poses different risks from bank lending. In order to properly grasp the risks of P2P lending, it is necessary to carefully analyse its structure and legal arrangements. In particular, depending on the legal arrangement, the failure of a P2P lending platform could lead to unexpected losses for its investors. For the sound development of P2P lending, those risks to investors must be mitigated.

This paper will first analyse the structure of P2P lending and its characteristics using traditional lending by banks as a reference point. The paper will then illustrate how legal arrangements of P2P lending differ from country to country. Finally, it will discuss the issue of investor protection in the event of the failure of a P2P lending platform based on those differences.

Structure and characteristics of P2P lending compared with bank lending

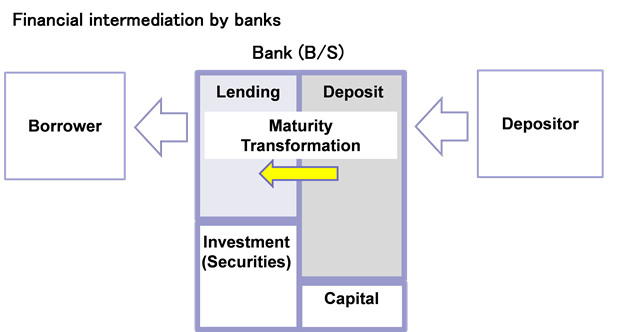

Banks engage in maturity transformation whereby they provide medium- and long-term loans to borrowers while raising funds through deposits. On the other hand, P2P lending is "direct lending between lenders and borrowers online outside traditional financial intermediaries like banks" (Atz and Bholat, 2016). P2P lending platforms match customers who have surplus funds with borrowers who are individuals or small and medium-sized enterprises (SMEs) via the Internet (Figure 1).

Figure 1: Financial intermediation by banks and P2P lending

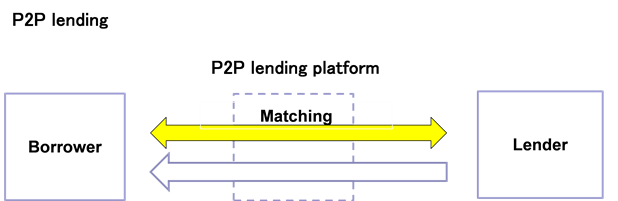

Similar to banks, P2P lending platforms assess borrowers' creditworthiness and monitor the credit risk of borrowers after loans have been extended. However, P2P lending differs from bank lending in that the lender, rather than the P2P lending platform, is responsible for deciding on whether to extend loans and for assuming the default risk of the borrowers (Figure 2). This is due to the fact that P2P lending platforms do not conduct business using their balance sheets in the way banks do. P2P lending platforms are therefore not subject to banking regulations such as capital adequacy requirements, leverage ratios, and liquidity requirements.

Figure 2: The main features of P2P lending platforms compared with banks

| P2P lending | Banks | |

|---|---|---|

| Assessing borrowers' creditworthiness | P2P lending platforms | Banks |

| Making loan decisions | Lenders | Banks |

| Monitoring borrowers after lending | P2P lending platforms | Banks |

| Taking on the default risk of borrowers | Lenders | Banks |

P2P lending and social welfare

P2P lending has the potential to improve social welfare by conducting business at a lower cost than existing financial intermediaries and distributing social surplus among lenders and borrowers. For instance, P2P lending is attractive to borrowers because of the relatively low interest rates and the speed at which borrowers can access funds compared to traditional bank loans. At the same time, P2P lending also benefits lenders by offering a higher yield than deposit rates under the current low interest rate environment.1

P2P lending might also improve social welfare because there is no systemic risk like that created by banks. First, P2P lending platforms do not have vulnerable balance sheet compositions. In other words, P2P lending platforms do not conduct business using their balance sheets in the way banks do, so there is no inherent risk on their balance sheets. Second, P2P lending businesses are not structured in a way where the collapse of one platform would lead to the collapse of others in a chain reaction. In other words, (i) P2P lending platforms are not required to refund lenders; (ii) P2P lending platforms do not take on the credit risk of counterparties; and (iii) unlike banks, which have interbank settlement functions, P2P lending platforms do not participate in deferred net settlement systems.

Systemic risk, however, has been re-defined more broadly as the potential of a widespread adverse effect on the financial system and thereby on the wider economy after the global financial crisis (IOSCO, 2011). According to this concept of systemic risk, the P2P lending market at present does not pose a systemic risk on the financial system. However, there are possible unfavourable developments which should be kept in mind. Regulators should pay attention to factors such as the size of the market, cross-border activities, interconnectedness through the involvement of institutional lenders or securitisation, and slippage in underwriting standards (Kirby and Worner 2014, IOSCO 2017).

- In P2P lending, lenders bear the default risk of borrowers. Therefore, the yield of P2P lending includes the credit costs which would be borne by the bank in the case of a bank loan. As long as P2P lenders can accommodate the borrowers' default risk, those high yields are beneficial for the lender.

Differences in legal arrangements for P2P lending in the UK, the US and Japan

While the structure and characteristics of P2P lending can generally be summarized as above, the legal arrangements of P2P lending differ from country to country. This article will explain the different legal treatments of P2P lending under the UK, the US and Japanese legal systems.

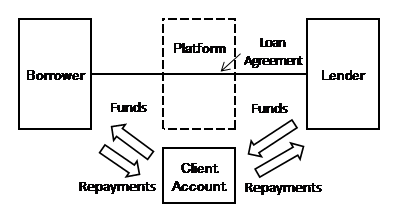

In the UK, a lender and a borrower enter into a direct loan agreement. The P2P lending platform matches lenders and borrowers, and it also collects loan repayments on behalf of the lenders. All loaned funds from lenders and repayments from borrowers go into segregated client accounts of the P2P lending platform, and the other creditors of the P2P lending platform have no claims over the funds in those accounts in the event of the failure of the platform (Figure 3).

Figure 3: P2P lending arrangement in the UK

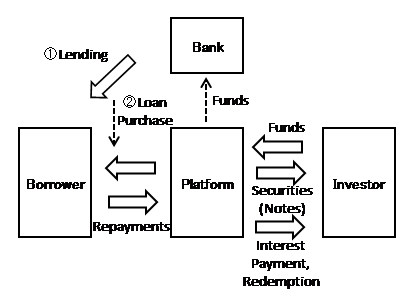

In the US, a loan agreement is not formed between the lender and the borrower. Rather, the P2P lending platform matches the lender and the borrower, and an affiliated bank of the P2P lending platform originates the loan. The P2P lending platform purchases the loans from the affiliated bank using funds raised from the sale of corresponding securities (notes) to investors (Figure 4).

Figure 4: P2P lending arrangement in the US

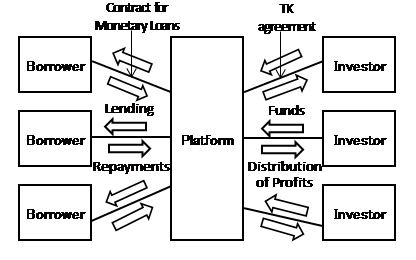

In Japan, too, lenders do not extend loans directly to borrowers. The P2P lending platform originates the loan with funds it collects from investors through silent partnership contracts (tokumei kumiai keiyaku: TK agreements) under the Commercial Code of Japan. Under those TK agreements, the P2P lending platform engages in lending as a business operator and the investors provide funds to the P2P lending platform as silent partners (Figure 5).

Figure 5: P2P lending arrangement in Japan

Analyses based on the differences in P2P lending legal arrangements

In the UK, since lenders and borrowers form direct loan agreements, the bankruptcy of a P2P lending platform would not necessarily lead to losses for the lenders. However there is a risk that the funds collected from the borrowers by the P2P lending platform will commingle with the property of the P2P lending platform. In addition, there is a concern that the loans will not be repaid due to a lapse in the administration of the loan. In this regard, the UK imposes segregation requirements on P2P lending platforms, and requires platforms to have arrangements in place to ensure that loans continue to be administered if the platform fails.

On the other hand, in the US and Japan, investors do not have direct claims to funds provided to or collected from borrowers. Therefore, the bankruptcy of a P2P lending platform could lead to unexpected losses for its investors. In particular, in Japan, funds provided by a silent partner (i.e., investors) are considered to be the property of the business operator (i.e., the P2P lending platform) (Article 536, paragraph (1) of the Commercial Code of Japan). Therefore, if a P2P lending platform fails, the investors would have only a general claim against the bankruptcy estate and would only be repaid pro rata with other general creditors.

In order to deal with the bankruptcy risk of P2P lending platforms in Japan, schemes such as specific purpose companies and specific purpose trusts can be used to segregate investors' loans from the other assets of the P2P lending platform. Such legal arrangements could strengthen investor protection in the context of the failure of P2P lending platforms, and could contribute to establishing confidence in the P2P lending market and its sound development.

Conclusion

This paper demonstrates that the legal arrangements of P2P lending vary from country to country, and those differences can affect the degree of investor protection. In the UK, where lenders and borrowers form direct loan agreements, lenders do not suffer losses so long as loans continue to be administered even in the case of a failure of a P2P lending platform. For this reason, the legal framework in the UK requires P2P lending platforms to have arrangements in place to ensure that loans continue to be administered by entering into an arrangement with another firm to take over the management of loan agreements in case of failure.

In considering whether new regulations need to be introduced in Japan, the current development of the P2P lending market and the treatment of P2P lending under the current legal framework for investor protection should be analysed, in particular as the size and the speed of growth of the P2P lending market differs in Japan and in the UK. In that regard, under the legal arrangements commonly used in Japan, the failure of a P2P lending platform poses risks that could lead to unexpected losses for its investors. This paper proposes the utilization of schemes such as specific purpose companies and specific purpose trusts to protect investors from those risks. It is important to encourage P2P lending platforms to utilize those schemes. At the same time, P2P lending platforms need to sufficiently explain the risks associated with P2P lending in light of the legal arrangements used, based on the current legal and regulatory disclosure requirements.2

- 2As for the disclosure of information to investors, it is important that P2P lending platforms provide investors with sufficient information to make decisions. It should be noted, however, that if P2P lending platforms provide detailed information on borrowers, that could undermine the protection of borrowers. Therefore, P2P lending platforms should ensure that borrowers remain anonymous when providing borrowers' information to investors (for example, in the UK, P2P lending platforms provide information such as sectors, regions, and delinquency status of borrowers).

References

- Atsushi Samitsu (2017), "The structure of P2P lending and legal arrangements: Focusing on P2P lending regulation in the UK," IMES Discussion Paper Series, No. 2017-J-3 (in Japanese).

- Carney M. (2017), "The promise of FinTech - Something New Under the Sun?," [PDF 712KB] (Link to an external website) Speech at Deutsche Bundesbank G20 conference on "Digitising finance, financial inclusion and financial literacy," 25 January 2017.

- Atz U. and Bholat D. (2016), "Peer-to-peer lending and financial innovation in the United Kingdom," [PDF 1,019KB] (Link to an external website) Staff Working Paper No. 598, Bank of England.

- International Organization of Securities Commissions (2011), "Mitigating Systemic Risk: A Role for Securities Regulators," [PDF 718KB] (Link to an external website) Discussion Paper OR 01.

- Kirby E. and Worner S. (2014), "Crowd-funding: An Infant Industry Growing Fast," [PDF 992KB] (Link to an external website) Staff Working Paper 3, International Organization of Securities Commissions.

- International Organization of Securities Commissions (2017), "IOSCO Research Report on Financial Technologies (FinTech)." [PDF 2.97MB] (Link to an external website)

Note

The views expressed herein are those of the author alone and do not necessarily reflect those of the Bank of Japan.