Summary of the Report of the Study Group on Legal Issues regarding Central Bank Digital Currency

Kenji Hayashi, Hiroyuki Takano, Makoto Chiba, Yasuhiro Takamoto (Bank of Japan)

Research LAB No.19-E-3, December 24, 2019

Keywords: central bank digital currency; CBDC; means of payment; central bank money; account-based; token-based; intermediating institution; legality; general acceptance; Bank of Japan Act; private law; administrative law; competition law; cyber law; criminal law

JEL Classification: G20, K14, K15, K21, K22, K23, K24

Contact: makoto.chiba@boj.or.jp

Summary

This article introduces the main findings of the Report of the Study Group on Legal Issues regarding Central Bank Digital Currency (CBDC). Based on four stylized models of CBDC issuance, the Report discusses what legal issues would arise within the Japanese legal framework if the Bank of Japan were to issue its own CBDC.

The Report finds a wide range of issues to be addressed. These include, among others, whether or not CBDC can be regarded as legal tender; what would happen in the case of counterfeit or duplication under current private law; whether or not issuance of CBDC is consistent with the purposes of the Bank as currently specified by the Bank of Japan Act; and whether the Bank can restrict the use of CBDC by certain individuals. The Report also discusses the legal issues related to the acquisition of information with respect to Anti-Money Laundering and Counter-Terrorism Financing (AML/CFT) regulations; protecting personal information; and the penalties for counterfeiting/duplicating CBDC as Crimes of Counterfeiting of Currency under current criminal law.

By clarifying these potential legal issues spanning various legal fields, the Report intends to stimulate further discussion regarding CBDC.

Introduction

CBDC has recently attracted increasing global attention. Academics have made various suggestions based on ongoing discussions. Central banks and international organizations have released reports examining the major issues regarding the implementation of CBDC. A few countries are already considering the possibility of issuing CBDC.

Ongoing discussions of CBDC are driven by developments in the financial environment. These developments include technological innovations in the financial sector, the transformation of payment services, and the declining use of cash. Increased awareness of financial inclusion may lend itself well to CBDC, especially in emerging economies. The appropriateness of CBDC issuance must be discussed from a wide range of perspectives, including the possible effects on financial systems and economies. Currently, most central banks, including the Bank of Japan, have made no plans to issue CBDC.

Nevertheless, given rapid changes in the financial environment, such as those triggered by information technologies, it seems worthwhile to initiate a thought experiment to identify potential legal issues that may arise from the issuance of CBDC in Japan. Such analysis will also contribute to deepening our understanding of the functions of currency in general, as well as the relationship between central bank money and commercial bank money.

Against this backdrop, the Bank of Japan's Institute for Monetary and Economic Studies commissioned the Study Group on Legal Issues regarding Central Bank Digital Currency to examine the issues surrounding the issuance of CBDC in Japan.

Models for CBDC Issuance

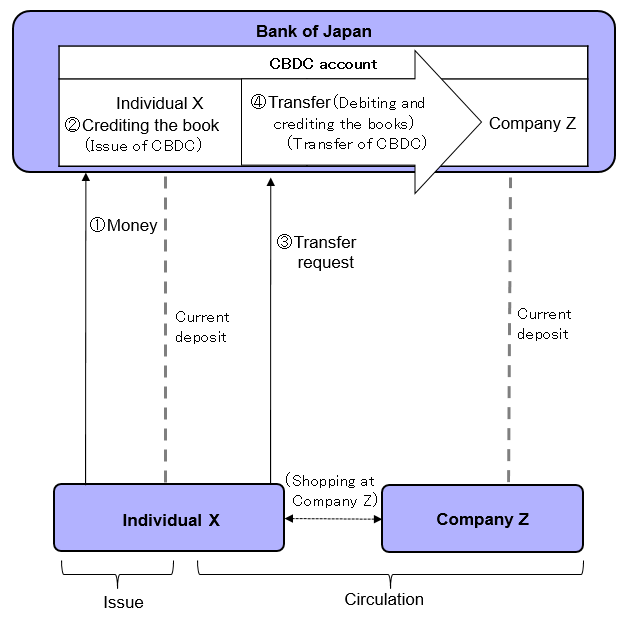

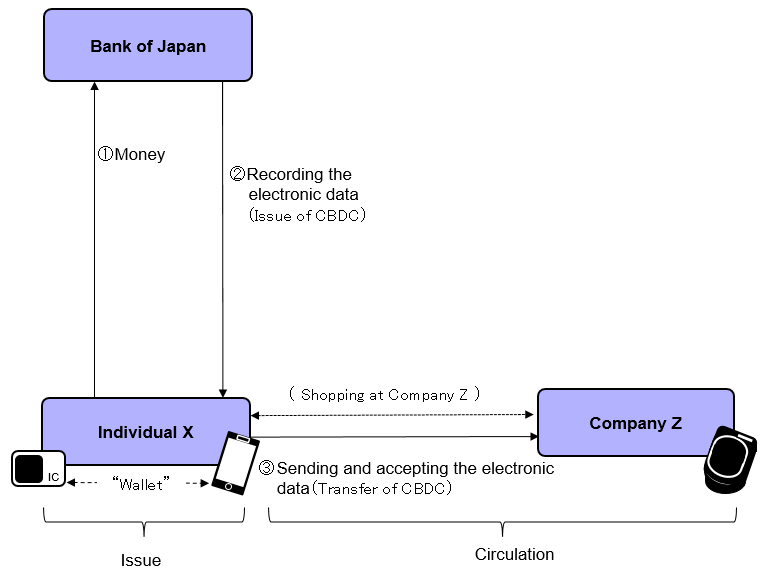

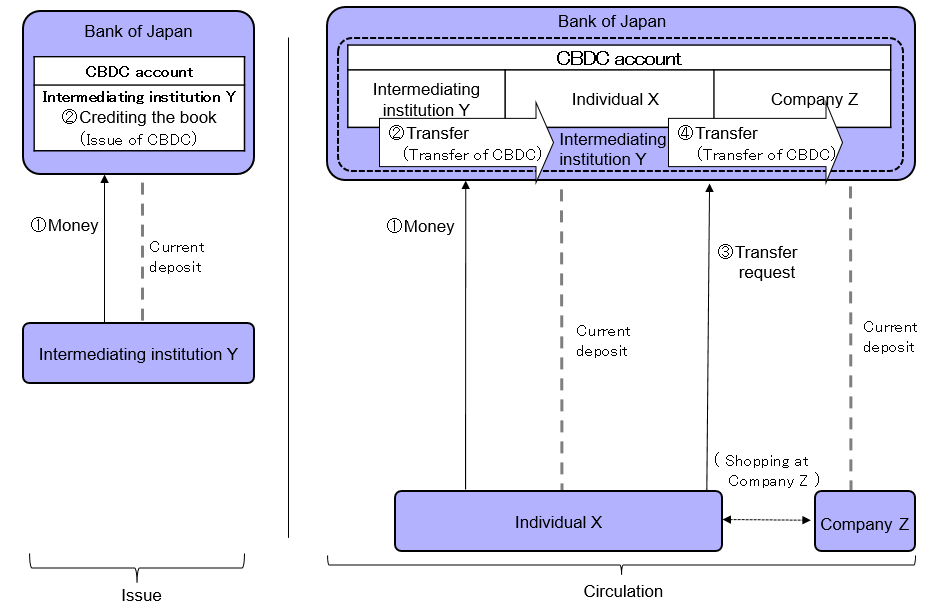

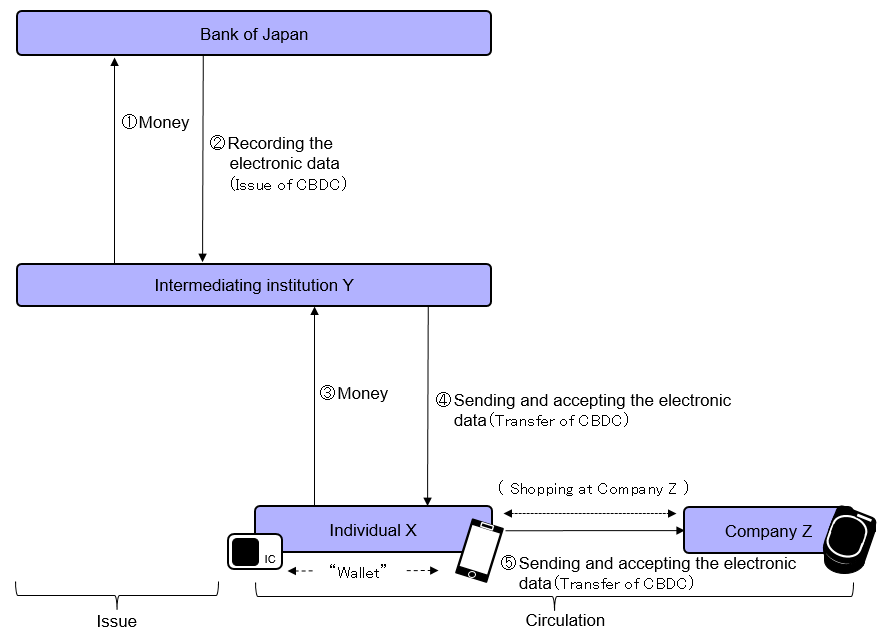

Prior to investigating potential legal issues, the Report assumes four stylized models of CBDC issuance based on the combination of account-based or token-based CBDC and direct or indirect provision (figure 1).

The Report also makes the following common assumptions across these models: (i) the Bank issues CBDC as central bank money, which is recorded on the Bank's balance sheet as its debt, (ii) the Bank continues to issue banknotes, and (iii) CBDC is mutually exchangeable for cash and private bank deposits, as well as for financial institutions' current deposits with the Bank.

Account-based versus token-based CBDC

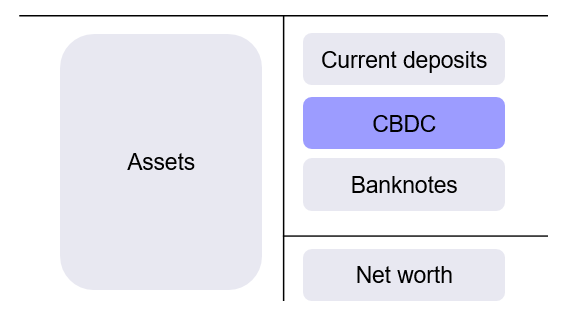

The Bank of Japan currently provides two forms of central bank money as a means of payment: current deposits and banknotes. Current deposits held with the Bank are deposit claims which are used for settling large-value transactions between financial institutions. Banknotes are paper media in which monetary value is incorporated. They are widely circulated among individuals and companies through private banks as a means of payment for retail transactions (figure 2).

Along with these two forms of central bank money, the Report assumes two types of CBDC.

The first type is account-based CBDC. This is regarded as allowing access to deposits for general users, such as individuals and companies, instead of limiting them to financial institutions. Legally speaking, account-based CBDC is the same as current deposits, that is, deposit claims, although they are general users' claims (not only financial institutions' claims) against the Bank. CBDC as deposit claims is transferred by debiting and crediting the books for deposits upon a transfer request from a general user.

The second type is token-based CBDC. This can be regarded as the digitalization of banknotes. However, the media in which monetary value is incorporated is not paper, as is the case for banknotes, but electronic data, which is recorded on dedicated instruments such as a smartphone or a smart/chip card ("wallet" in figure 1). Token-based CBDC is transferred by sending and accepting this electronic data.

Direct versus indirect provision of CBDC

CBDC can be provided by the Bank to general users either directly or indirectly. In the latter case, CBDC is supplied from the Bank to intermediating institutions, from which it is widely distributed to general users.

Since the current tiered financial and payment system consists of a central bank and commercial banks, direct provision of CBDC would have a profound effect on this system as a whole, including the possibility of decreasing the intermediation process of commercial banks. At the same time, it would certainly increase operational costs of the Bank, which would need to handle an enormous number of users. Indirect provision, in contrast, may to some extent address these issues.

Selected Legal Issues

Based on the above four stylized models, the Report examines in detail a number of concerns to be addressed should the Bank begin issuing CBDC. Below is a summary of its main findings.

CBDC as legal tender

The current legal framework in Japan does not stipulate any legal tender other than banknotes and coins. Thus, legislation would be required in order to make CBDC legal tender. Whether or not that legislation would automatically guarantee the general acceptance of CBDC as currency is a separate issue, as that would depend on the credibility of CBDC.

Counterfeiting/duplicating and losing CBDC data under private law

In principle, payment using counterfeited or duplicated data is invalid irrespective of whether CBDC is account-based or token-based. In practice, however, it may be difficult or even impossible in real time to identify which one of any duplicated data is authentic. In that case, due procedure could be established, for example, to process the payment by treating all data as authentic for the moment and to claim for damages against the duplicator afterwards.

Even if the data of account-based CBDC is lost, for example by accident, the deposit claim itself remains intact, from a legal point of view. Users could therefore claim a refund of CBDC. On the other hand, if the data of token-based CBDC is lost, the monetary value is deemed to have disappeared. That is, in principle, a user could not claim for reissuance of CBDC.

Foreclosure of CBDC under private law

The foreclosure of account-based CBDC could be handled in line with the existing process of foreclosing deposits with private banks, as it is the same as deposit claims. In contrast, the foreclosure of token-based CBDC requires further discussion regarding the process of how to foreclose data. There has not been sufficient consensus or discussion on this matter within the current Japanese legal framework.

The Report also raises a number of issues related to current private law, such as the timing of transfers and rules against unlawful acquisition of CBDC.

Consistency with purposes specified by the Bank of Japan Act

The Article 1, Paragraph 1 of the Bank of Japan Act stipulates that, "The purpose of the Bank of Japan, the central bank of Japan, is to issue banknotes and to carry out currency and monetary control." The Act has a provision prescribing the printing and cancellation of banknotes. This provision assumes that a banknote is a tangible artifact. It is therefore difficult to assume that "banknotes" includes intangible CBDC. This implies that the issuance of CBDC is not contained within the purpose defined in Paragraph 1 of the Bank of Japan Act.

Article 1, Paragraph 2 of the Act also stipulates that "…the Bank of Japan's purpose is to ensure smooth settlement of funds among banks and other financial institutions, thereby contributing to the maintenance of stability of the financial system." It seems that the issuance of CBDC may not be covered by this purpose either, as CBDC would be used for settlement among the general public, beyond financial institutions. In this regard, there might be room for interpretation such that the smooth settlement of funds among the general public helps achieve the ultimate purpose of the maintenance of stability of the financial system. Such an interpretation however raises further questions, including how to avoid possible conflict with retail payment services provided by the private sector.

Meanwhile, there is an argument related to administrative law that the core elements of public sector administrative activities must be based on solid legal grounds, irrespective of whether or not such activities could involve the infringement of rights. According to this argument, any change to the core elements of the Bank's activity, such as the launch of CBDC, should be clearly specified by law.

Restrictions on the use of CBDC under competition law

Under competition law, the Bank, as the monopolistic provider of CBDC, would be obliged to fulfill any transaction demands of general users. Nonetheless, there might be cases in which it would be better for the Bank to restrict transactions by certain users and financial intermediaries in order to fulfil the Bank's purpose and ensure efficient operations. For example, the Bank may need to exclude some users under AML/CFT regulations. The Bank may also need to exclude unqualified business operators in order to ensure the stability of payment and settlement systems. The Bank would have to provide reasonable justification for the imposition of such restrictions, as well as for conditions such as fees and transaction upper limits.

Information acquisition under AML/CFT regulations

The Act on Prevention of Transfer of Criminal Proceeds, which prescribes the current AML/CFT regulations, requires private banks to verify identities, store transactions records and notify suspicious transactions regarding their deposit contracts with customers. In extending AML/CFT regulations, these requirements may also apply to CBDC transactions. If CBDC is provided indirectly, intermediating institutions conduct operations such as identity verification. In that case, the design of institutional arrangements determines who bears legal responsibility when an intermediary violates AML/CFT regulations. It may be the Bank's responsibility, if the intermediary is operating under the auspices of the Bank; or it may be the intermediary if it carries out these operations as its own business.

Protecting personal information

The Bank would acquire individual transaction information through CBDC. This includes information on individual attributes such as the name and birthdate of the individual; payments such as the amount of payment and payment date; and commerce such as the name of goods/services purchased and their unit prices. If CBDC is provided indirectly, the Bank may not acquire this information, depending on the nature of the contracts with intermediating institutions.

Even information on payments and commerce constitutes "personal information" under the personal information protection legislation, if a specific person can be identified by connecting that information to individual attributes. If it possesses this information, the Bank becomes responsible for its appropriate management.

Meanwhile, the appropriateness of using individual transaction information needs to be considered, not only in light of personal information protection but also in terms of fair competition under competition law.

Crimes of Counterfeiting of Currency under criminal law

Currently under the Penal Code, the object of the Crimes of Counterfeiting of Currency is defined as "a current coin, bank note or bill." CBDC thus cannot be an object of these crimes. It may be the case that counterfeiting/duplicating of CBDC may fall under Crimes related to Electromagnetic Records of Payment Cards or Crimes concerning Unauthorized Creation of Electromagnetic Records. However, the statutory penalties for these crimes are lighter than those for Crimes of Counterfeiting of Currency.

If the law were amended so as to include counterfeiting/duplicating of CBDC under Crimes of Counterfeiting of Currency, it would be essential to take into account the special features of digital currency, such as the ease of counterfeiting/duplicating on a large scale for a short time. Moreover, given that counterfeiting/duplicating of digital currency issued by the private sector is not covered by Crimes of Counterfeiting of Currency, the question arises as to why CBDC and private sector digital currency are treated differently in this respect.

Conclusion

There is a wide range of potential legal issues that may arise from CBDC issuance. These issues span a broad range of legal fields, including both private and criminal law, the Bank of Japan Act, legislation on data collection, and administrative and competition law. Some of these issues need to be addressed by legislation. Before launching CBDC, more detailed discussion is needed to further clarify the legal issues. Like other institutional arrangements regarding CBDC, the legal framework would vary depending on the purpose of CBDC issuance.

By clarifying the potential legal issues, the Report intends to stimulate further discussions regarding CBDC.

Figure 1 : Models of CBDC (image)

-

(Model 1) Account-based CBDC and direct provision of CBDC

-

(Model 2) Token-based CBDC and direct provision of CBDC

-

(Model 3) Account-based CBDC and indirect provision of CBDC

-

(Model 4) Token-based CBDC and indirect provision of CBDC

Figure 2 : Bank of Japan's balance sheet (image)

Reference

Study group report on "Legal Issues regarding Central Bank Digital Currency" (2019), to be included in Kin'yu Kenkyu (Monetary and Economic Studies), Institute for Monetary and Economic Studies, Bank of Japan (forthcoming 2020) (available in Japanese only).

Note

The views expressed herein are those of the authors and do not necessarily reflect those of the Bank of Japan.